TBW - Crypto market faces liquidity crunch

The party seems to be over, for a while at least. In the space of a few weeks, Bitcoin has lost more than 20% of its value, falling below the symbolic $100,000 mark in early November before stabilising at around $105,000. Ethereum and Solana have suffered even more, falling 30% and 41% respectively since their highs for the year.

This correction comes amid widespread nervousness. The rise in real rates and the Federal Reserve's perceived more restrictive tone have dampened risk appetite. Fed Chairman Jerome Powell hinted that October's rate cut could be the last of the year, signalling a return to monetary caution.

Equity markets retreated, dragging down digital assets, which are often correlated in phases of macroeconomic stress.

But the real turning point came a month earlier. On 10 October, a message posted on Truth Social by Donald Trump announcing 100% tariffs against China triggered a flash panic: more than $19 billion of crypto positions were liquidated in a few hours, an all-time record according to CoinGlass.

This episode, now dubbed the "10/10 crash", left deep marks on the market.

>> The black weekend that shook cryptos

A liquidity mechanic jammed

Beyond cyclical volatility, a more structural phenomenon is emerging: the slowdown in liquidity. In a note published on 5 November, market maker Wintermute reminds us that "technological adoption may carry the long-term narrative, but it is liquidity that really moves prices". Since the spring, the three main channels feeding the market (stablecoins, ETFs and Digital Asset Treasuries) have been showing signs of running out of steam.

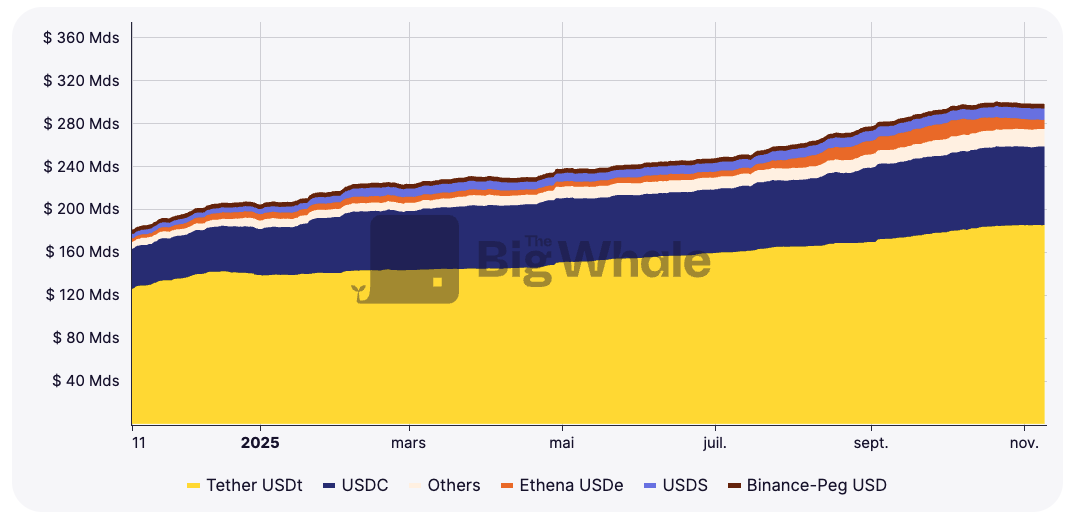

These instruments are the main gateways for capital to enter the ecosystem. Stablecoins embody on-chain liquidity and serve as collateral for derivatives markets. Crypto ETFs channel institutional and passive flows from traditional finance. Digital Asset Treasuries (DATs), finally, are a kind of tokenised funds that link traditional assets to on-chain liquidity.

According to Wintermute, these three channels expanded rapidly between early 2024 and mid-2025: DATs and ETFs grew from around $40 billion to $270 billion, while total stablecoin outstandings doubled to almost $290 billion. But the momentum has since slowed considerably. "Liquidity has not disappeared, it is simply circulating within the system rather than expanding it," explains the trading company.

In other words, capital is not leaving the market, but it is no longer being added to it. Rotations take place between Bitcoin, Ethereum and altcoins, with no net influx of new investors.

>> Market makers' techniques for manipulating markets

A self-financing economy

This situation reflects what Wintermute calls a "self-financing" phase, where the market turns on itself. Existing funds move from one asset to another, causing short-lived rises and sharp corrections. Volumes remain high, but market depth is reduced, making liquidations more violent and rallies shorter. This phenomenon is accentuated by the behaviour of long-term holders.

Many of those who subscribe to the theory of Bitcoin's four-year cycle are selling their positions, convinced that we are close to the top.

For the time being, the macroeconomy is not coming to the cryptos' rescue. The global money supply is still expanding, but money prefers other playgrounds, notably the equity markets. Continued high short-term rates are encouraging investors to keep their cash in Treasuries rather than deploy it in risky assets. Cryptos, once the great beneficiaries of periods of easing, now find themselves deprived of external fuel.

Signals of a future upturn

To emerge from this phase of stagnation, external flows will have to return. Wintermute identifies several signals to watch: a resumption of stablecoin issuance (an indicator of on-chain demand for collateral), new crypto ETF creations, synonymous with renewed institutional interest, and a revival of DATs.

Each of these channels reflects a distinct liquidity driver: speculative demand for stablecoins, institutional demand via ETFs and demand for yield through DATs. Their synchronisation propelled the market to 2024-2025. Their simultaneous slowdown now signals the end of the expansion cycle.

But this pause is not necessarily a bad sign. It may allow the market to consolidate, integrate the accumulated gains and prepare for the next wave. If monetary conditions ease again, the fuel of liquidity could return sooner than we think.

>> Discover our Bitcoin Dashboard