TBW - Digital Assets Treasuries (DATs): a good bet, really?

This analysis was carried out in collaboration with Castle Labs.

Introduction

Digital Asset Treasuries (DATs) - or digital asset treasuries - have become an increasingly popular mechanism for attracting interest from traditional finance (TradFi) into major crypto-assets such as Bitcoin (BTC) and Ethereum (ETH).

We are now seeing a wave of companies whose thesis is based on the accumulation of digital assets on their balance sheets, in the form of strategic reserves.

The DAT model allows investors to gain exposure to crypto via an equity-type vehicle: they do not hold the tokens directly, but buy shares in a company that holds them on its balance sheet.

DATs can also be seen as an institutional wrapper for crypto-assets, avoiding the need for investors to manage the (often complex) custody of their tokens themselves, or to go through exchange platforms that are potentially vulnerable to hacks and data leaks.

The main player in the sector, Strategy (formerly MicroStrategy), holds around 640,000 BTC, or nearly 3% of the total Bitcoin supply.

its success - and soaring share price ($MSTR) - has made the model attractive to other companies looking to raise capital and buy digital assets in turn.

These purchases change the amount of tokens held per share, fuelling speculation on the net asset value per share (mNAV) and premiums or discounts on the stock.

This report aims to explain the internal workings of DATs, their main indicators, the companies involved, the associated risks and their long-term sustainability.

What is a DAT and how does it work?

The term Digital Asset Treasury (DAT) was born alongside Strategy's transformation from a simple data analytics software company into a DAT in August 2020.

Since that pivot, its share value has soared by more than 2,000%.

This success is not just due to its pioneering status in Bitcoin buying, but demonstrates the viability of the DAT model as a business opportunity.

A DAT acts as an equity-funded accumulation vehicle: it raises funds, buys crypto-assets, and increases the exposure of its balance sheet to these assets.

its key valuation indicators - NAV, mNAV, premium/discount - depend directly on the performance of the asset(s) held.

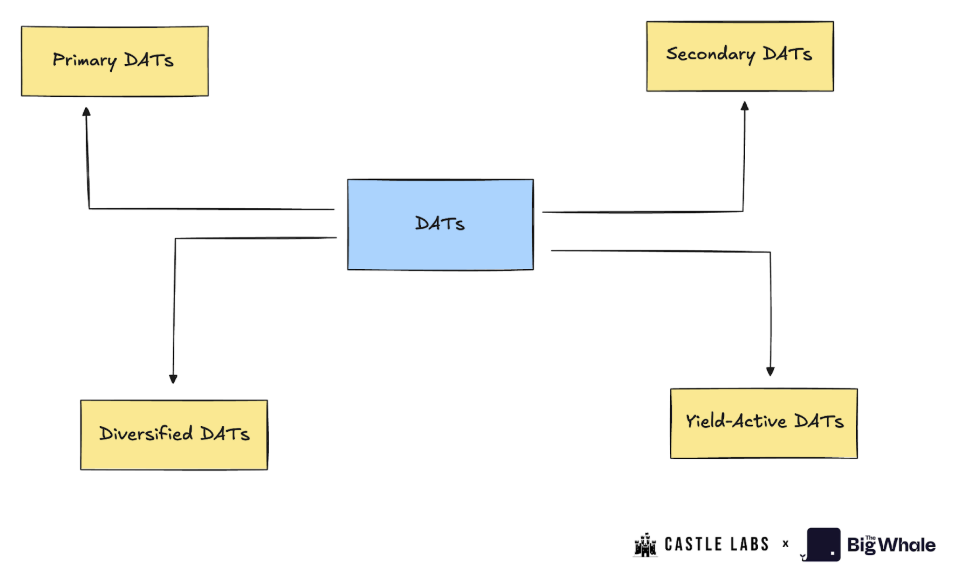

Typology of DATs

DATs can be classified into several categories:

1. Primary DATs

These are the "pure" DATs, which raise funds via share issues to accumulate a given asset (often Bitcoin or Ethereum).

Examples: Strategy, BitMine.

2. Secondary DATs

These do not follow the pure DAT model and derive part of their valuation from ancillary activities.

These companies generate operational revenues which they then reinvest in crypto-assets.

Examples: Tesla, Galaxy Digital, Marathon Digital (MARA).

3. Yield-active DATs

These companies seek to generate yield from their crypto-assets (staking, DeFi, etc.).

Example: Sharplink, which bets and remunerates the majority of its holdings in ETH.

4. Diversified DATs

They hold several types of digital assets (BTC, ETH, SOL, ADA, etc.) to diversify their exposure.

Examples: Nepute Digital Assets Corp (BTC, ETH, SOL) and BTCS Inc (ETH, ADA, SOL).

Although these sub-categories differ in their strategies, this report focuses on a few representative cases to illustrate the dynamics of the sector.

Key DAT terminology

To understand the inner workings of a Digital Asset Treasury, it is necessary to master a few fundamental indicators that help assess their financial health and performance.

1. Net Asset Value (NAV)

The NAV corresponds to the total value of a DAT's crypto cash, calculated by multiplying the number of assets held by their dollar value.

For example, if a DAT holds 10,000 BTC and each Bitcoin is worth $114,000, its NAV amounts to $1.14 billion.

2. NAV per share (NAVps - Net Asset Value per Share)

This is the NAV divided by the total number of shares outstanding (adjusted for dilution).

It indicates how much a share should be worth based on DAT holdings.

If the share price is above this value, it trades at a premium; otherwise, at a discount.

3. Crypto per share (CPS - Crypto Per Share)

This indicator expresses the number of units of crypto (BTC, ETH, etc.) that each share represents.

It therefore measures the shareholder's "indirect right" to the stock of tokens held.

4. Market NAV ratio (mNAV)

The mNAV compares a company's market capitalisation to the value of its cash in digital assets.

- If mNAV > 1, the stock is trading at a premium - investors pay more than book value for liquidity, leverage or an access option.

- If mNAV < 1, the stock is trading at a discount - a sign of scepticism, governance risks or a lack of transparency.

5. Accretion/Dilution Test

This test is used to determine whether a share issue is beneficial (accretive) or harmful (dilutive) to shareholders.

A transaction is accretive when:

(\Delta U / \Delta S) > (U / S)

- ΔU = new tokens purchased

- ΔS = new shares issued

- U and S = tokens and existing shares

Example:

A company raises $1bn, its stock trades at a 40% premium (mNAV = 1.4), and it holds 200,000 BTC (NAV = $22bn) for 20 million shares.

Share price: $1,540 → issue of 650,000 shares.

With the funds raised, it buys a further 9,000 BTC (at $110,000).

→ New total: 209,000 BTC.

→ CPS before: 200k / 20M = 0.01

→ CPS after: 209k / 20.65M = 0.0101

The issue is slightly flow-through.

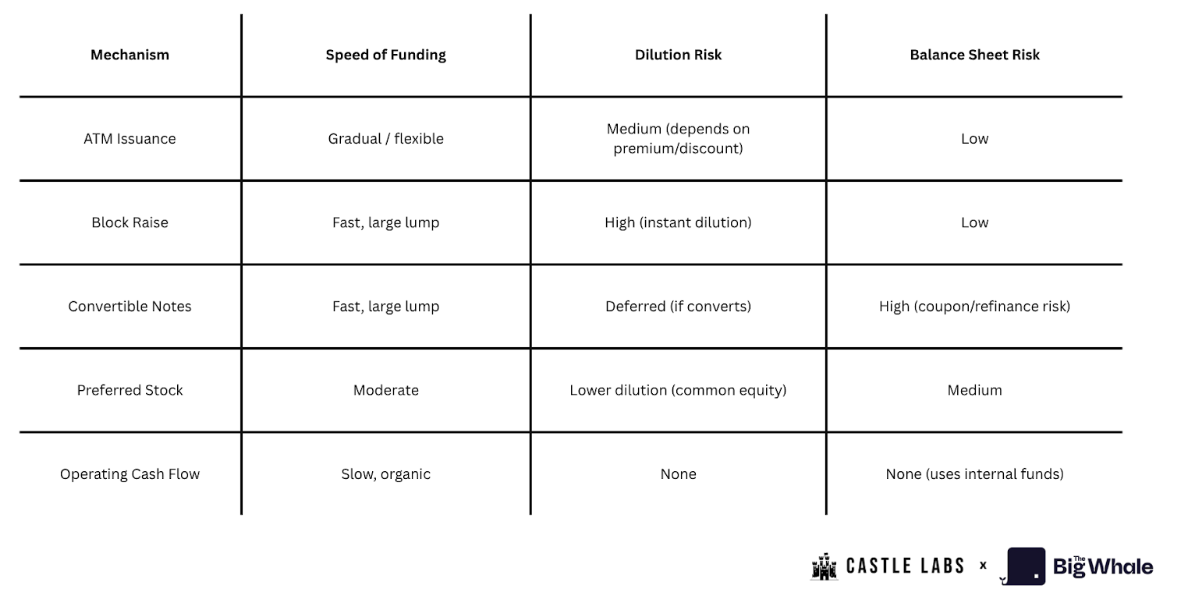

DAT financing mechanisms

Companies adopt different strategies to finance their crypto-asset purchases:

1. "At-the-Market" issues (ATM)

The DAT sets up a programme with an investment bank to gradually sell its shares on the market, then use the funds to acquire digital assets.

This mechanism only works when the share is trading at a premium to NAV.

This is a flexible, low-friction tool, but potentially dilutive if overused.

2. Block / Secondary Issues

The company issues a massive block of shares at a price slightly below the market, in order to quickly raise funds to buy crypto-assets.

Advantage: quick cash inflow.

Disadvantage: immediate dilution of existing shareholders.

3. Convertible notes (Obligations convertibles)

The DAT issues debt securities with a fixed interest rate, a maturity, and an option to convert into shares at a predefined price.

This mechanism allows financing without immediate dilution, but introduces two risks:

- If the share price rises above the conversion price → dilution at term.

- If the share price falls → the debt remains due, creating a refinancing risk.

4. Preferred Stock

These securities give priority over ordinary shares on dividends and liquidation.

They reduce the cost of capital, but create a hierarchy between shareholders, limiting the earning potential of traditional shareholders.

5. Operating Cash Flow (OCF)

A healthier method is to reinvest a portion of operating profits into the purchase of crypto-assets.

This is the least dilutive but also the slowest way to build cash.

>> Bitcoin Treasury Companies : An overview of the financial levers at their disposal

The current landscape of DATs

The growing institutional appetite for digital assets has led to the emergence of a diverse ecosystem of listed companies seeking to capitalise on one of the great financial narratives of 2025: the transformation of capital into crypto-currency.

First focused on Bitcoin, the model quickly expanded to Ethereum, Solana and other leading blockchains.

In most of these companies, the central objective remains the same: to increase the amount of digital assets held per share.

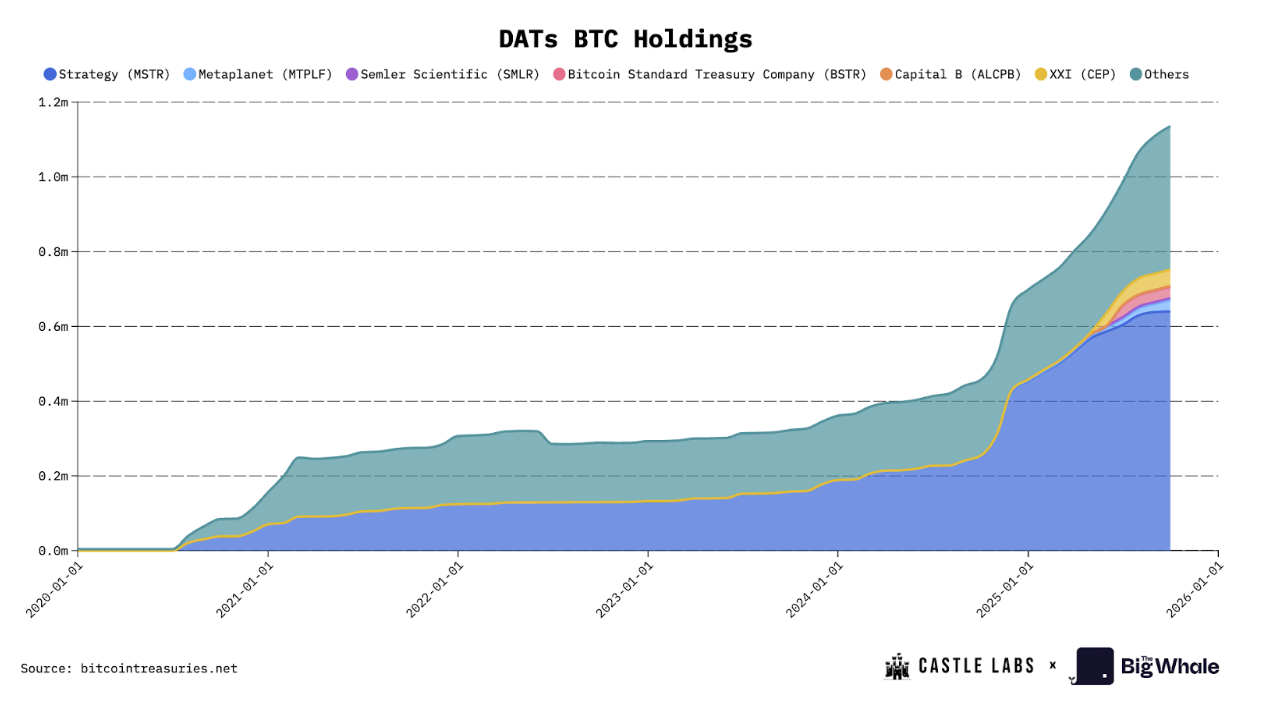

The DATs studied in this section represent the majority of assets under management (AUM) among listed companies holding BTC or ETH.

Strategy and Metaplanet together hold 64% of the total AUM of all listed Bitcoin DATs, with Strategy alone holding 61.22%.

On the Ethereum DAT side, BitMine accounts for 49.66% of AUM in the ETH segment, and Sharplink 14.72%.

This concentration indicates a clear dominance of the first entrants, capable of raising capital quickly.

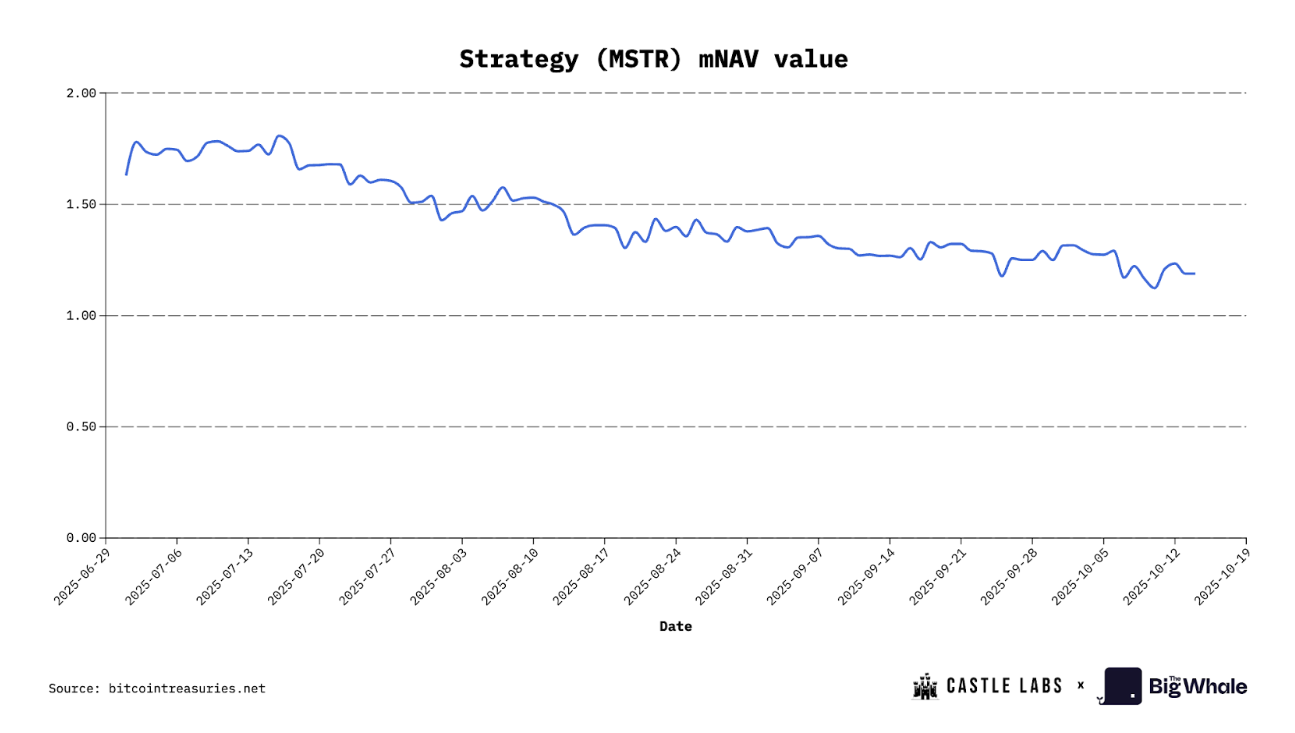

Strategy: pioneering the DAT model

Launched in 2020, Strategy (formerly MicroStrategy) inaugurated the listed digital treasury model.

In five years, the company has accumulated 640,250 BTC, valued at around $70 billion at current prices.

In 2025, it bought 116,554 bitcoins, a 26% return on its BTC stock.

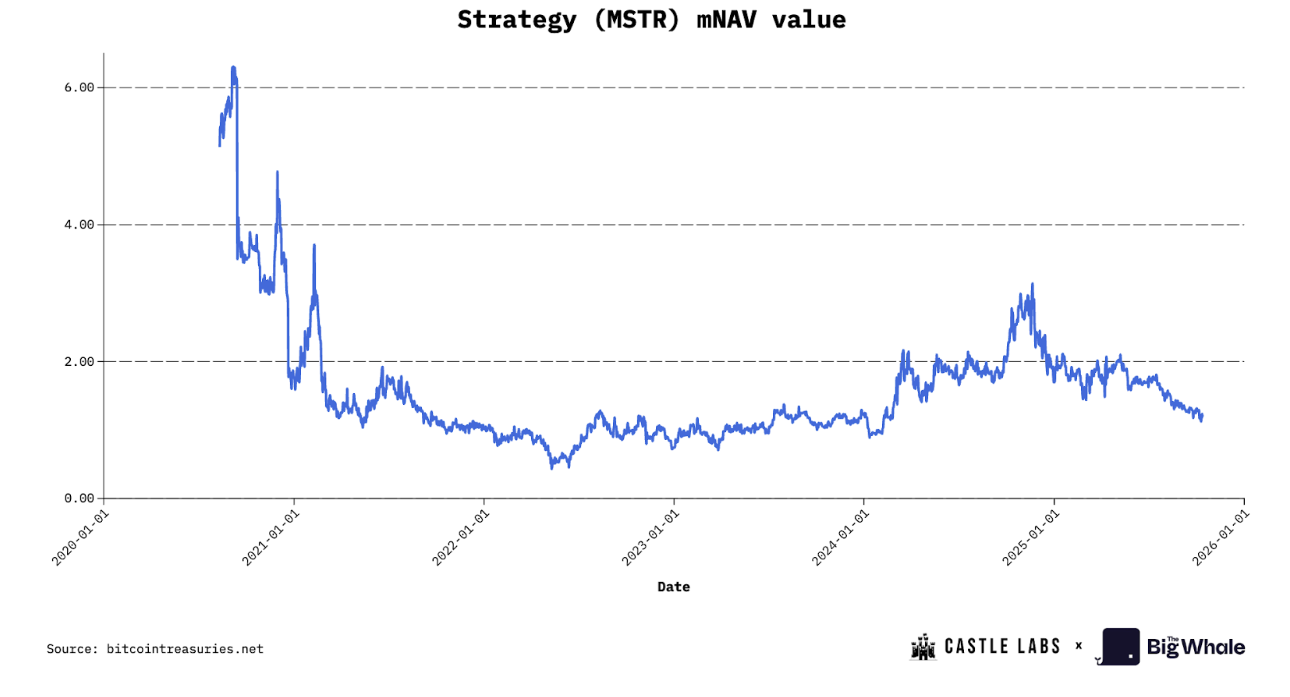

Strategy has primarily relied on the ATM (At-the-Market) model to fund its acquisitions, selling its shares at a premium of up to 6x net asset value in its early days.

This multiple has since fallen sharply:

- first to around 2.5x-3x,

- then below 1.5x,

- before stabilising around an mNAV of 1.16x (basic) and 1.293x fully diluted.

Preference shares and convertible bonds are now the dominant financing instruments.

These products, largely absorbed by hedge funds and institutional investors, enable BTC's acquisitions to be maintained while limiting immediate dilution.

Thanks to its pioneering advantage and recognition on global stock markets (almost eligible for the S&P 500), Strategy remains the benchmark in the sector.

But this status also implies a systemic risk: a Strategy failure would have a tectonic impact on investor confidence - both in equity markets and in the "Bitcoin as a reserve asset" narrative.

Metaplanet: the Japanese reinvention

Another major player, Metaplanet - a former Japanese hotel company - has converted to digital asset management and now holds more than 30,823 BTC.

Benefiting from an exceptional stock market premium (up to 8x NAV at one point in the year), the company has been able to raise eight times more capital than the value of its BTC holdings.

This is due to its listing on the Tokyo Stock Exchange, which attracts Japanese investors seeking exposure to Bitcoin's volatility.

For many local investors, Metaplanet represents an indirect means of investing in BTC via a listed product, more accessible than foreign platforms.

>> Strategy, XXI, Metaplanet, The Blockchain Group: The Comparative of Bitcoin Treasury Companies

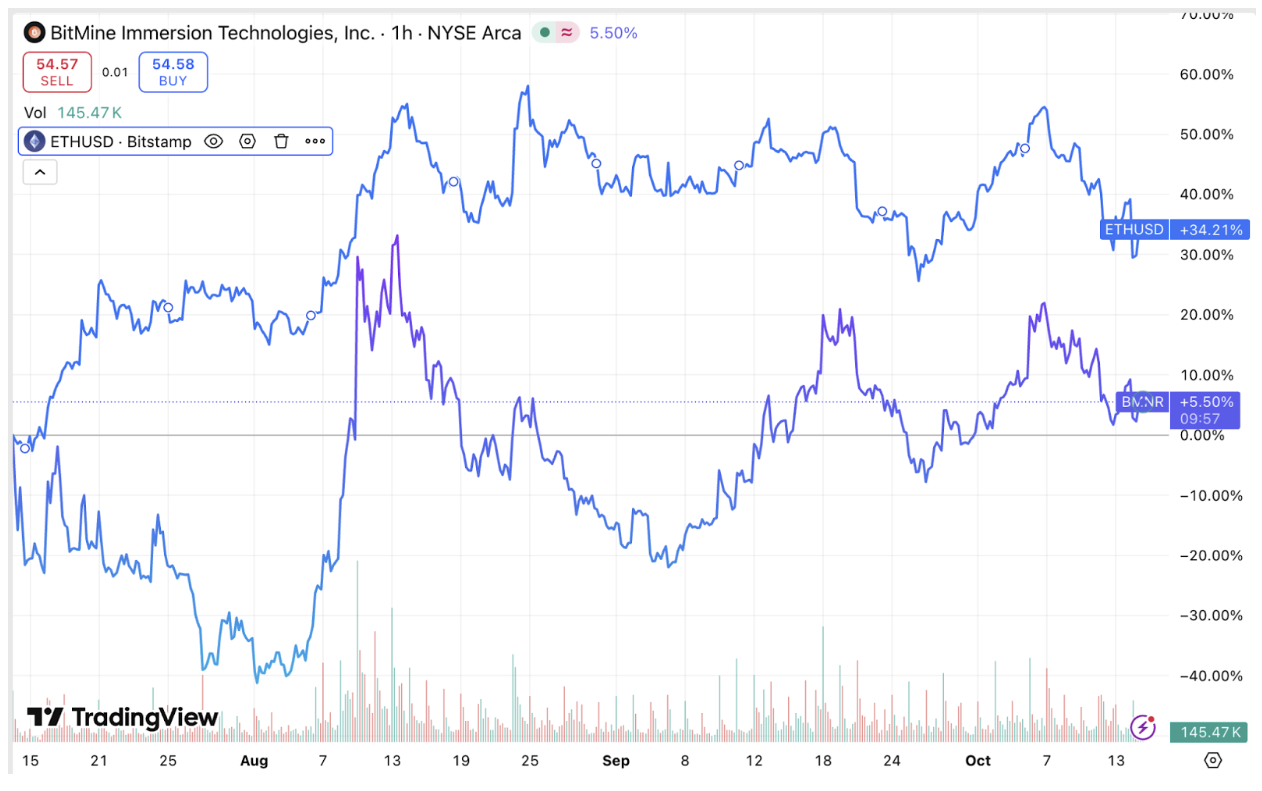

BitMine and Sharplink : The pioneers of the corporate ETH

On the Ethereum side, two players dominate the market:

- BitMine, originally a Bitcoin mining company converted to an Ethereum DAT in July 2025,

- and Sharplink, a company that originated in sports marketing and pivoted to the DAT model.

Between them, they hold more than 3.87 million ETH, totalling more than $15 billion.

Their earnings per share are 189.1% for BitMine and 98.5% for Sharplink, respectively.

Like their Bitcoin counterparts, they favour raising capital via ATM programmes, selling their shares as long as a market premium exists.

This allows them to raise funds efficiently without resorting to debt or massive issues, while maintaining growth in the number of ETH per share (CPS).

But as soon as the premium disappears - when the mNAV falls below 1 - the mechanics become dilutive.

Currently:

- Sharplink is trading at a slight discount (mNAV = 0.92x),

- while BitMine retains an 18% premium (mNAV = 1.18x).

The ETH staking advantage

ETH treasury companies have an advantage that their Bitcoin equivalents do not:

they can stake their holdings to generate a native return of around 3 to 3.5%.

This return contributes directly to increasing the ETH value per share, without the need to issue new shares.

Some companies, such as Sharplink, even reinvest staking rewards in DeFi protocols or share buyback programmes, partially offsetting the dilution caused by ATM sales.

A model that's still young, but growing

Aside from Strategy, most DATs are still at an early stage of development.

Aggressive capital raisings demonstrate their desire to take advantage of the current bull cycle to build a bridge between traditional finance and digital assets.

The risks of the DAT model

The key element attracting capital to DAT shares is their net asset value (mNAV) multiple.

Speculators buy these stocks to amplify the returns of the underlying crypto-assets: they hope to multiply their gains by 1.5x to 7x on every dollar invested.

But behind this attractive mechanism lies a paradox:

investors are not buying Bitcoin or Ethereum, but a volatility wrapper whose value depends entirely on the level of premium or discount on the mNAV.

These investment vehicles carry many risks, often misunderstood by the general public.

1. Massive shareholder dilution

One of the major risks of the DAT model is the ongoing dilution associated with the share issues required to fund crypto purchases.

Between 2022 and the end of 2024, Strategy diluted its shareholders by nearly 46% per year on average.

For Metaplanet, the projected dilution for 2025 is even more spectacular, reaching 98%!

As for Ethereum DATs:

- BitMine shows an estimated dilution of 24.25%,

- Sharplink at 11.4% (calculated quarter on quarter).

These high levels are the direct consequence of ATM programmes, which allow shares to be issued as and when they are needed as long as the share price remains above NAV.

The operating cash flows of these companies are also largely negative:

- Strategy: -$34 million in Q2,

- Sharplink: -$1.62 million in Q2.

Denied organic cash inflows, they must continually raise capital to maintain their accumulation strategy - a viable approach only as long as the market values the premium.

When the stock goes into a discount, the mechanism jams: the company can no longer raise without becoming heavily diluted, leading to stagnation in the number of assets per share and a downward spiral effect on the share price.

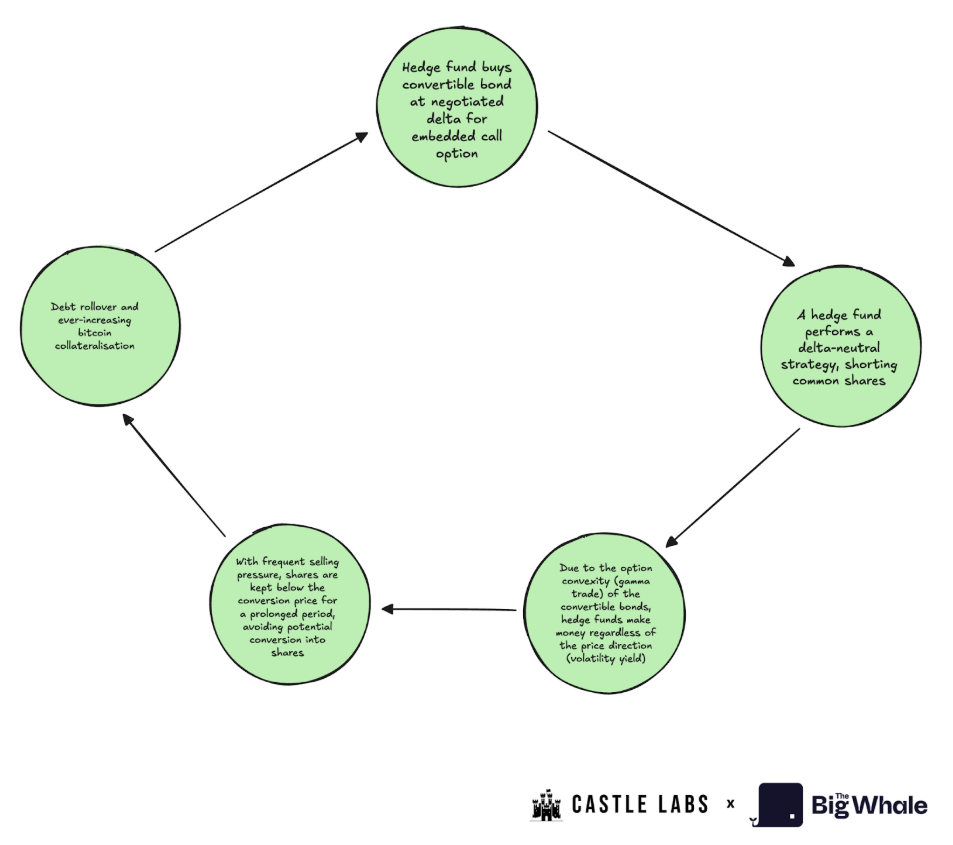

2. Convertible debt: a dangerous game

To avoid dilution too quickly, some companies - Strategy in particular - have resorted to convertible bonds.

These securities are very popular with hedge funds, as they include an embedded call option that allows them to benefit from the stock's volatility.

The typical operation is as follows:

- The funds buy the convertible bonds,

- They open a short position on the stock to hedge,

- And exploit the stock's volatility to generate delta-neutral returns.

This mechanism creates a vicious circle: as volatility increases, the value of the bond appreciates, but at the cost of constant selling pressure on the share.

If the price approaches the conversion price, the "delta" of the product increases, amplifying speculation.

In the event of a fall, the funds benefit from their short position, while the value of the bond remains supported by the collateralised assets (the BTC held).

This strategy, known as "bond convexity", turns DAT shares into volatility instruments whose oscillations hedge funds exploit, without any real fundamental conviction about the company.

Their ideal scenario: perpetual rollover of convertible debt, as long as volatility remains high and the market continues to absorb new issues.

3. Preference shares: a false solution

Another mechanism invented by Strategy: the issue of preference shares.

These securities are intended to reduce dilution without increasing debt, but in return offer fixed dividends to holders - an additional burden for companies whose cash flows are already in deficit.

Their use exacerbates the financial fragility of DATs, which struggle to generate cash to meet these payments.

4. Governance and liquidity risks

Beyond the capital structure, other risks threaten the stability of the DAT model:

- Lack of transparency on holdings: companies rarely publish the public addresses of their portfolios, which prevents an independent audit.

- Risk of executing share buyback programmes, which are often announced without the necessary liquidity.

- Risk of liquidity: in the event of a forced sale (eg. Liquidity risk: in the event of a forced sale (e.g. market crash), it would be difficult for a DAT to liquidate its assets without causing a fall in prices.

- Internal sales: executives regularly sell their shares, increasing the pressure on the stock.

5. Growing underperformance

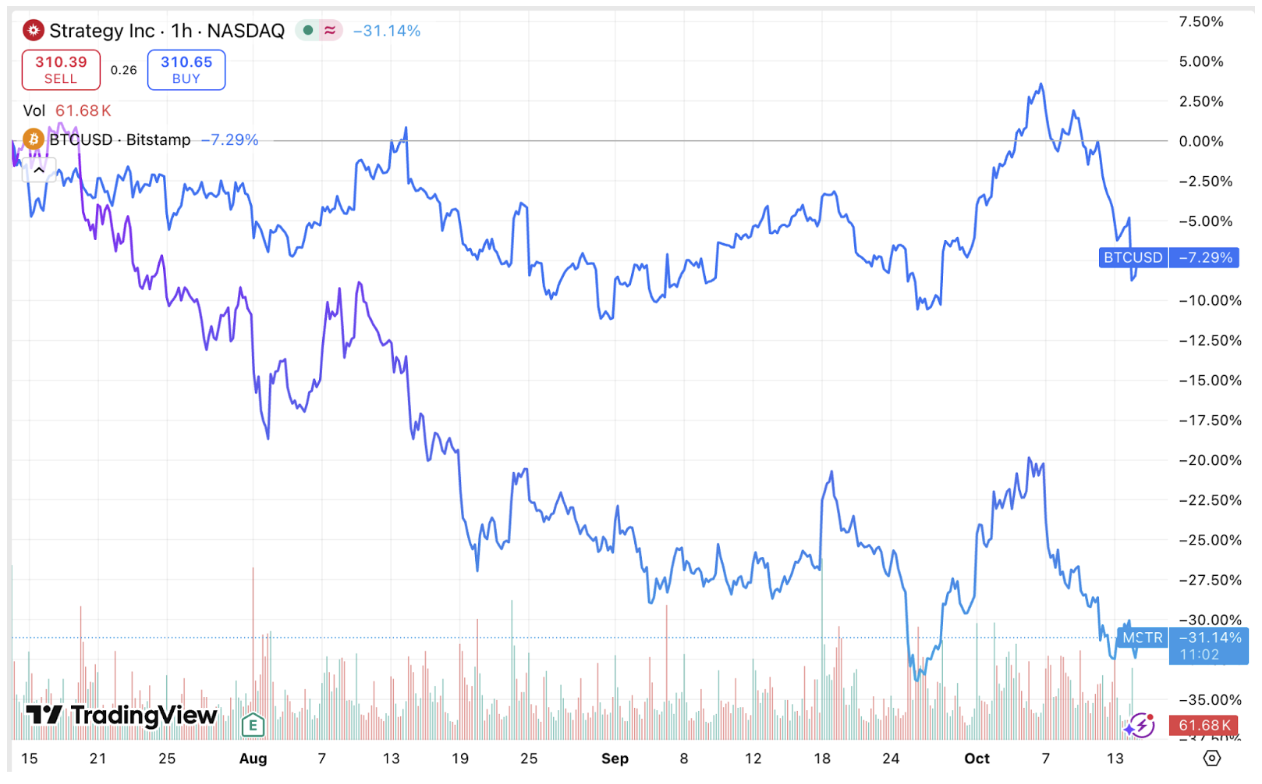

Since the middle of the year, most DATs have seen their market capitalisation plummet:

- MSTR has lost 44% of its value,

- Metaplanet more than 70%.

These declines reflect a general disenchantment:

investors anticipate an end to the expansion cycle, and now see these securities as underperforming the underlying assets (BTC or ETH themselves).

In other words, DATs, which had served as speculative relays for the market's rise, are now victims of their own leverage.

This growing disconnect between equities and the crypto they represent raises the question of their medium-term structural viability.

>> Strategy: Michael Saylor's black scenario

DATs beyond Bitcoin and Ethereum

Holding Ethereum in cash allows companies to generate a native return through staking, currently around 3.18% per annum.

This yield helps to gradually grow the ETH value per share, which improves the intrinsic performance of DATs.

But even leveraging the strongest DeFi protocols, it would take years for staking to compensate for continued dilution if capital does not grow in tandem.

Revenues from staking and yield farming remain marginal and insufficient, at current scale, to support operational expenses and enrich shareholders.

Theoretically, a yield-oriented DAT could be self-sustaining if:

- it accumulates a critical volume of crypto-assets;

- the yield generated covers its operating costs and increases wealth per share.

In practice, this remains very difficult: dependence on asset valuation remains total.

The success of an "ETH" DAT therefore depends as much on the price of Ether as on market demand for this type of product.

Currently, Bitcoin DATs (like Strategy) are enjoying stronger investor appetite - a reflection of the perception of BTC as a "hard" and more stable monetary asset.

Markets have moreover already incorporated the risk inherent in these vehicles, explaining the growing performance gap between DAT shares and the crypto-assets they represent.

Over the third quarter, the returns on Bitcoin and Ethereum far outstripped those on their exchange-tokenised versions (MSTR, SBET, etc.).

The very model - based on the purchase of assets as the core business - limits the creation of intrinsic value:

cash is not productive, cash flows are negative, dividends weigh on the balance sheet, and debt is increasing.

The result: a gradual erosion of valuation multiples for the majority of DATs.

Example of a missed opportunity: "John the investor"

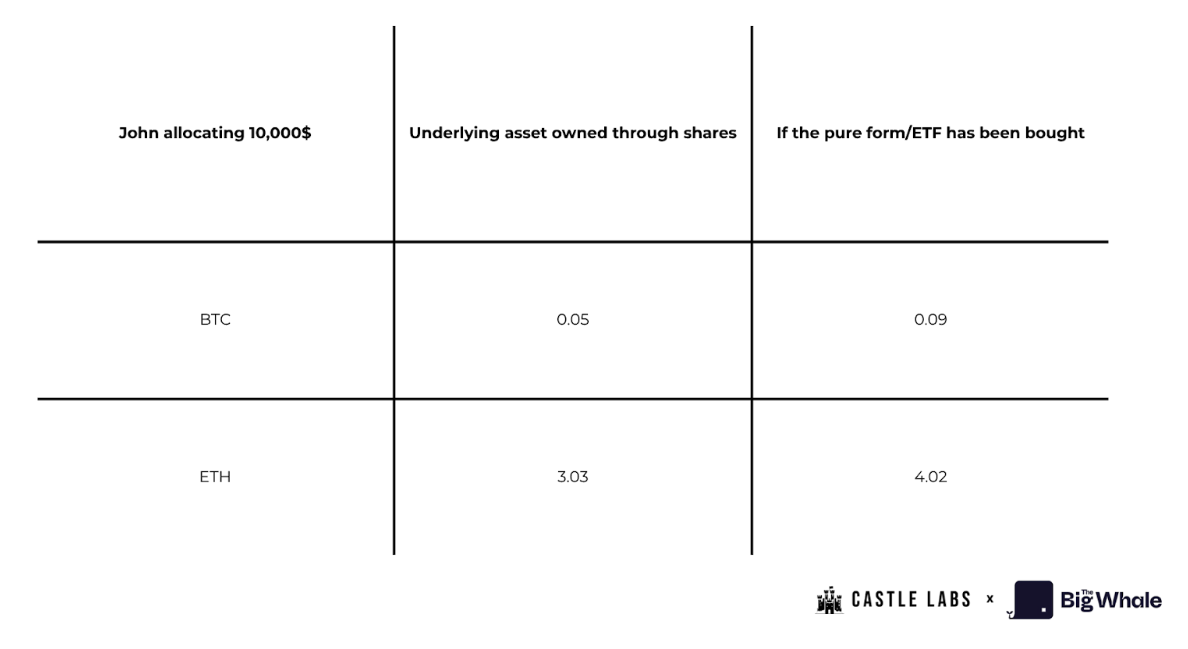

Let's imagine John, an individual investor with $10,000 to invest at the end of June (Q2).

He has two choices:

- buy BTC or ETH directly ("pure" form or via ETF),

- or invest the same amount in DAT shares (MSTR for BTC, SBET for ETH).

If he chooses pure assets:

- he gets 0.093 BTC or just over 4 ETH.

If he chooses DATs:

- 24.6 MSTR shares,

- 1,065 SBET shares.

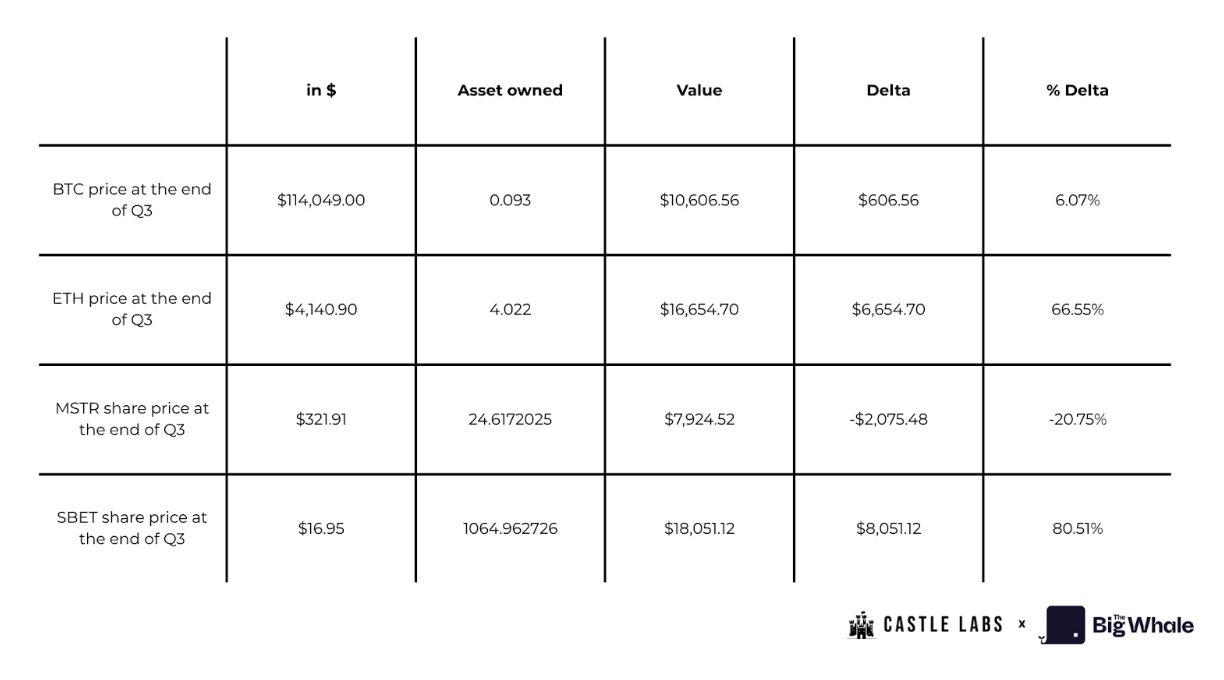

At the end of the following quarter (Q3), the result was mixed:

- In quantity of crypto per share, John would hold 0.04 BTC less than if he had bought Bitcoin directly.

- In ETH, he would have one Ether less than via the cash purchase.

But in terms of value, the trajectories diverge:

- Sharplink's (SBET) share price appreciated by +80%, earning him around $8,000 in profit,

- While MSTR fell by -20.75%, reducing his position by $2,000.

This comparison illustrates the high opportunity cost of DATs: retail investors own no underlying assets and depend exclusively on the stock market behaviour of the company.

In the event of bankruptcy, creditors and holders of preference shares take precedence over ordinary shareholders in claiming crypto reserves.

This severely undermines the credibility of the model as a long-term investment vehicle.

A model dependent on derivatives markets and volatility

The accounting profits claimed by some DAT companies are often illusory: US FASB standards allow them to recognise unrealised gains on their holdings as income, even if these assets are not sold.

These profits therefore remain purely "on paper" and do not generate real cash flows.

To make the model sustainable, companies should:

- invest part of their holdings (lending, covered options, etc.) to generate returns,

- diversify their revenues to reduce dependence on the BTC/ETH price.

But each new DeFi integration increases counterparty and security risks, raising the question: is it worth the risk?

The prevailing market perception remains clear: if these players start selling their assets, it would be seen as a major warning signal, precipitating investor distrust.

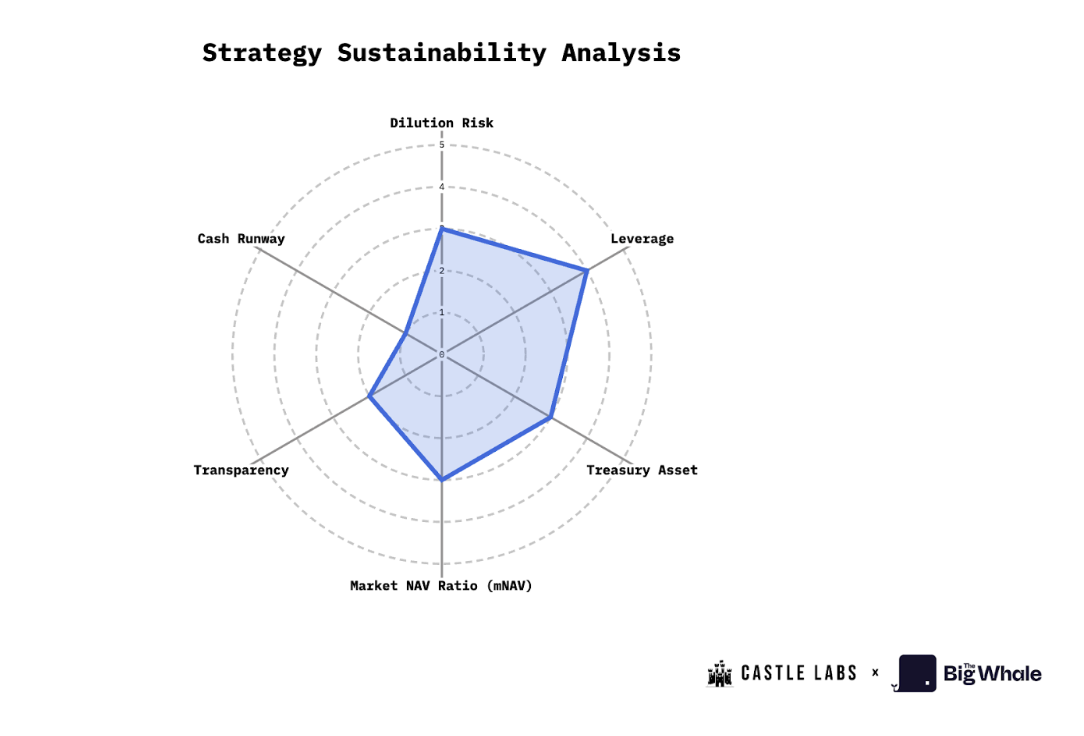

Assessing the sustainability of the model

Although no single indicator can perfectly capture the performance of a DAT, there are several measures that can be used to assess its long-term soundness and viability.

This section uses the case of Strategy (MSTR) to illustrate how these criteria can be applied and scored on a scale of 0 to 5:

a score of 4 or more reflects good performance, 3 indicates average performance, and 2 or less signals structural weakness.

Dilution risk

Dilution risk arises when the issue of new shares reduces the amount of crypto held per share (CPS).

If the exercise allows more crypto to be purchased per share than before, it is said to be accretive; otherwise, it is dilutive.

In Strategy's case, the company has regularly used ATM share issues and convertible bonds to finance its BTC purchases.

As long as the share was trading at a premium (mNAV > 1), these issues could be considered broadly accretive.

But the structural reliance on these fundraisings places Strategy in a low to moderate dilution risk category, a score of 3 out of 5.

.png)

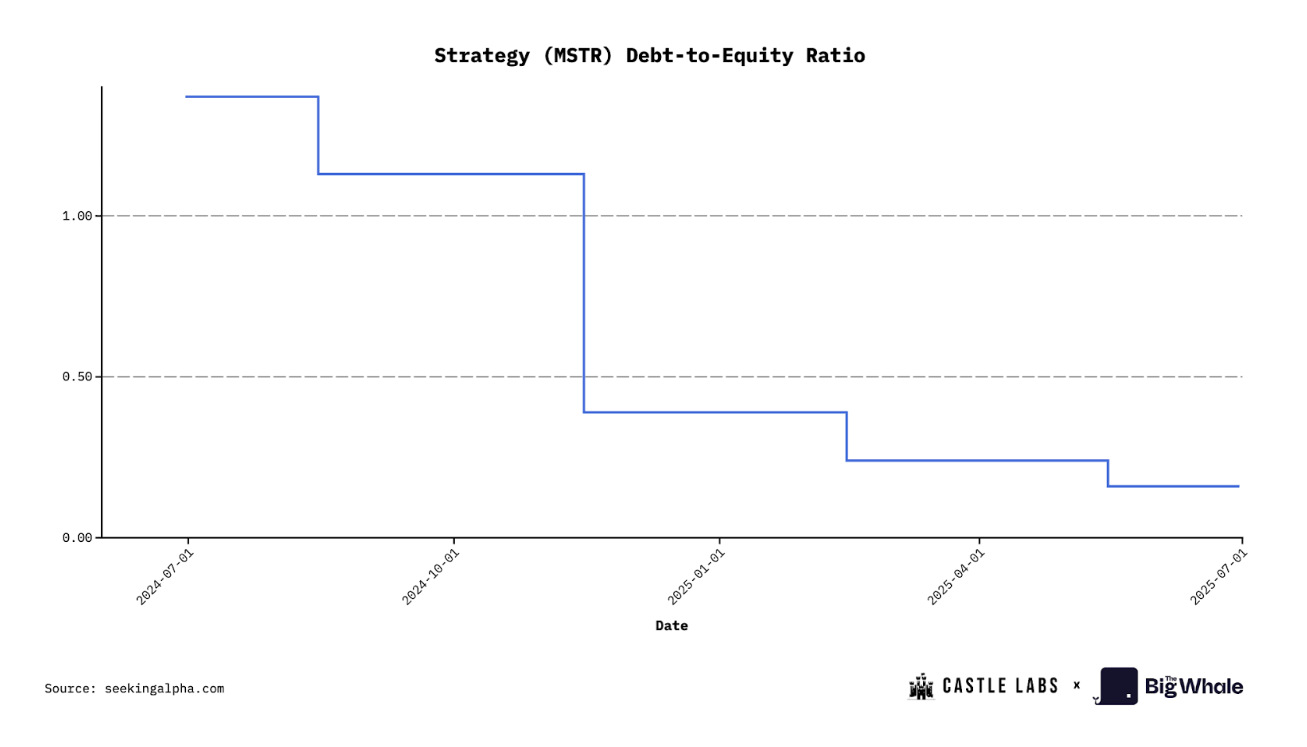

Leverage

To measure the leverage of a DAT, we need to assess the proportion of debt used to buy digital assets.

This debt can take the form of convertible bonds, secured loans or other hybrid instruments.

The debt-to-equity ratio provides an indication of whether a fall in the value of the digital treasure could create a liquidity crisis.

At Strategy, this ratio is currently at its lowest level since the model was created, at around 0.36.

This places the company in the low leverage category, corresponding to a score of 4 out of 5.

Quality of assets held

The nature of the assets a company holds is a key factor in judging its strength.

Most DATs focus on "blue chip" assets such as BTC, ETH or SOL.

Ethereum stands out for its ability to generate a steady staking return (around 3% a year), which can be used to fund operations or bolster cash flow.

For example, a DAT holding $1bn in ETH could generate nearly $30m a year in staking income, or more if it participates in lending or liquidity protocols.

However, these opportunities come with increased counterparty risk.

Bitcoin, on the other hand, does not generate an active return, but derives its value from its scarcity and its role as a monetary reserve.

Since Strategy exclusively holds BTC, a robust but non-performing asset, it falls into a medium category, scoring 3.

Multiple NAV Ratio (mNAV)

The mNAV is one of the simplest and most revealing indicators for evaluating a DAT.

It corresponds to the company's market capitalisation divided by the value of its crypto cash.

For Strategy, the current capitalisation is $82.3 billion, compared with an estimated NAV of $70 billion, giving an mNAV of 1.16 in the basic version and 1.25 in the fully diluted version.

According to the reference scale:

- an mNAV greater than 1.2 is considered good (score 4 or 5),

- between 1.0 and 1.2 as average (score 3),

- between 0.8 and 1.0 as poor (score 1 or 2),

- below 0.8 as bad (score 0).

Strategy is therefore in the middle, with a score of 3.

Transparency and governance

This indicator, which is more qualitative, measures the frequency and quality of information published by the company concerning its treasury, audits and proof of reserves.

Some companies choose not to disclose the public addresses of their portfolios to avoid being front-runnered when making purchases.

But this lack of transparency fuels investor scepticism.

Strategy is often criticised for voluntarily limiting the transparency of its reserves and the complexity of its governance structure (multiplicity of instruments: preference shares, convertible bonds, etc.).

It therefore gets a score of 2 out of 5.

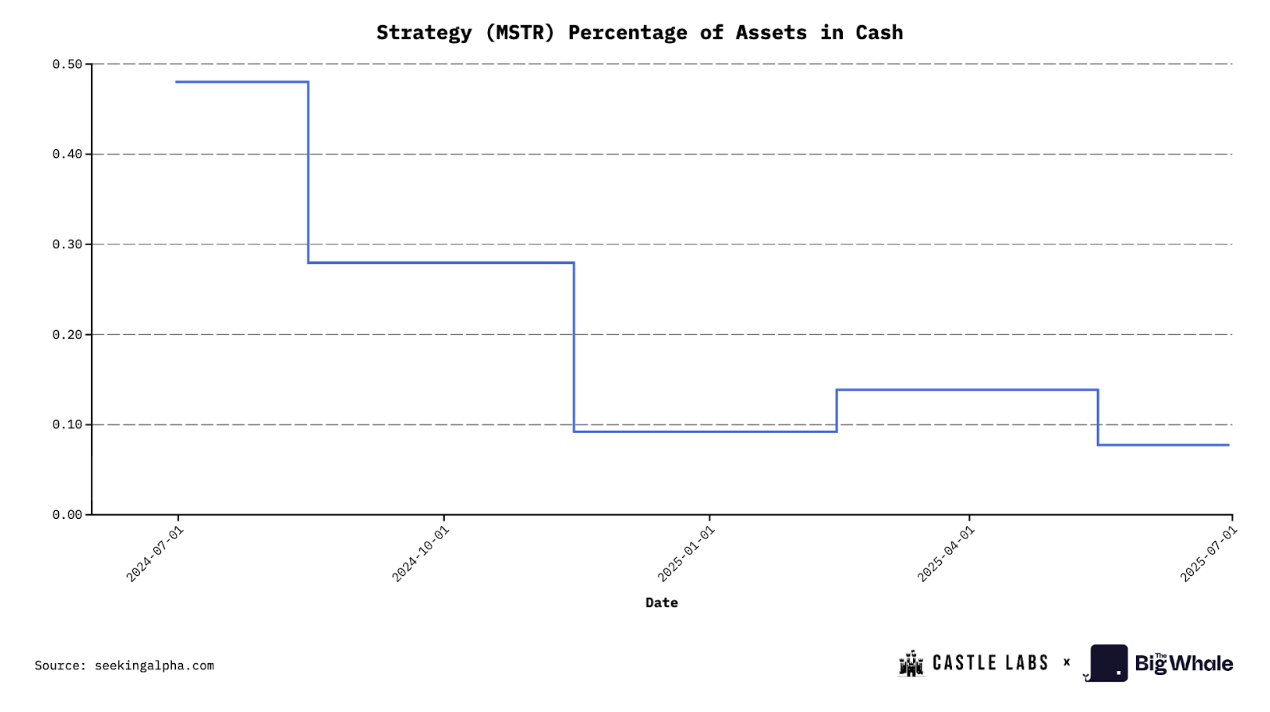

Liquidity and available cash

Finally, it is crucial to assess a DAT's ability to meet its current expenses without having to sell its digital assets.

This "cash runway" can be estimated by dividing monthly expenses by available cash.

A company with a year's worth of cash is considered solid.

At Strategy, cash represents just 0.07% of its total assets - an extremely low level.

This gives it a score of 1, illustrating an almost total reliance on Bitcoin's valuation to maintain its operations.

Average score: 2.83 / 5

Overall, Strategy achieves an average score of 2.83 out of 5 across these six categories: dilution risk, leverage, asset quality, mNAV, transparency and cash.

This assessment reflects a structurally sound but operationally fragile business, dependent on both the Bitcoin market and investor confidence.

Conclusion

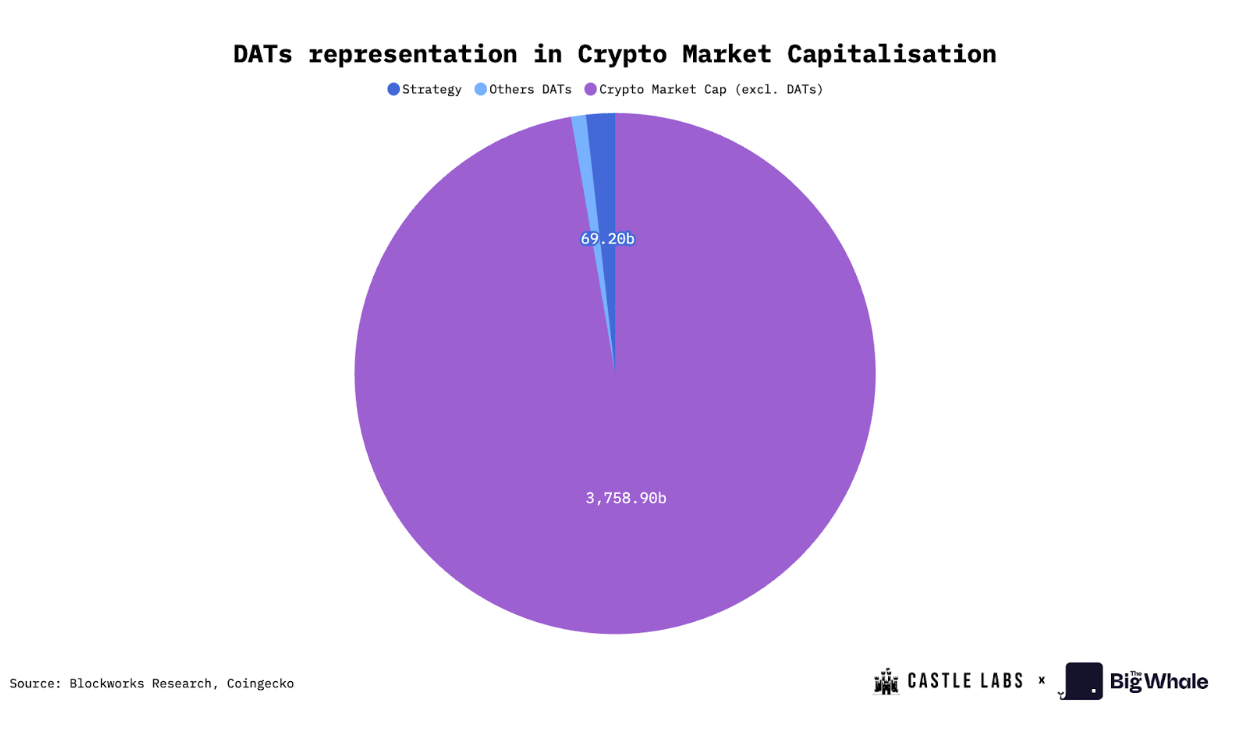

Digital Asset Treasuries have taken a notable place in the crypto industry, with a cumulative net value of around $108 billion, or 2.5% of the total cryptocurrency market capitalisation.

By themselves, these companies now represent an intermediate asset class between technology equity and direct exposure to Bitcoin.

Their main attraction: allowing investors to gain indirect exposure to crypto, without portfolio management, by betting on valuation differentials (premiums/discounts) between the stock and the underlying assets.

But the model is now reaching its limits:

- permanent dilution weakens shareholders,

- revenues remain low or even negative,

- debt is accumulating,

- and dependence on market cycles is total.

DATs now extend beyond top-tier assets like Bitcoin and Ethereum, including Solana and other L1 assets. These additional assets allow DATs to increase their leverage, as they can be used to generate returns on their holdings via DeFi. The return generated can be used to finance the company's operations or to improve economic indicators. For example, ETH staking increases the company's ETH reserves, which increases its ETH value per share, a key indicator that investors assess before investing in the stock.

The growth of these DATs and their key economic indicators are highly dependent on the prices of their underlying digital assets. In times of high market volatility, their mNAV can fall significantly.

At the end of the day, the proliferation of DATs and the increase in their NAVs also reflects increased institutional and retail interest in digital assets, which is positive for the sector. However, anyone investing in these vehicles should be aware of their risks, as mentioned in the report.

>> Report The Big Whale: Bitcoin Treasury Companies - Diving into a unique business model worldwide