TBW - From promises to reality: what crypto IPOs reveal

For the past few months, a number of companies specialising in digital assets have been taking the next step: listed markets. Exchanges, custody companies, fintechs and mining players... they are all rushing to file with the Securities and Exchange Commission (SEC) or to finalise an IPO.

A trend that illustrates the increasing integration of crypto into traditional financing channels and its gradual move towards mainstream financial infrastructure.

For expert Aram Mughalyan, these IPOs are a sign of renewed maturity. According to him, the Biden mandate and the hard line adopted by Gary Gensler at the SEC made any IPO virtually impossible, with the authority favouring a strategy with tough enforcement.

The arrival of Donald Trump in the White House has changed the game: the rhetoric is now "build with safeguards" rather than "sanction first". As a result, boards of directors finally have visibility, bankers have comparables and crypto companies can turn to public markets (something they had been unable to do for the past four years).

>> Omar Shakeeb and Oleg Ivanov (SecondLane): "All pre-IPO crypto companies are revalued upwards"

IPO pioneers

The first wave of crypto IPOs began back in 2017 with HIVE Blockchain Technologies. The Canadian company, which specialises in mining powered by renewable energy, led the way on the TSX Venture Exchange before joining the Nasdaq in 2021 (under the ticker HVBT). It now operates data centres in Iceland, Sweden and Canada.

Bakkt followed in 2018 with a different ambition: to connect the digital economy. Listed on the New York Stock Exchange (BKKT) since October 2021, its platform aims to create bridges between consumers, businesses and institutions, enabling crypto-assets and loyalty points to be used interchangeably.

The most emblematic case remains that of Coinbase, which entered the Nasdaq on 14 April 2021 after ten years of development and an already strong base of 56 million users. A symbolic milestone that marked the integration of crypto into the American financial landscape.

The same year, Robinhood made its debut on Wall Street. On 28 July 2021, the platform raised nearly $1.9 billion with an initial offering at $38 per share (HOOD). A few months later, Argo Blockchain, a British player in sustainable mining, in turn listed on Nasdaq (ARBK), raising $112.5 million with the backing of Jefferies and Barclays.

Expansion has not been limited to the historic crypto players. Brazilian fintech NU Holdings Ltd. completed a major IPO, raising the equivalent of 14.45 billion reais through an offering of nearly 290 million shares. More recently, eToro completed its IPO in May 2025. The deal, valued at $4.2 billion and backed by Goldman Sachs and Citigroup, saw the social trading platform raise around $620 million (ETOR).

The 2025 wave: Circle, Bullish, Gemini and the others

The year 2025 marked an unprecedented acceleration in crypto IPOs. On 5 June, Circle, issuer of the stablecoin USDC, took its first steps on Wall Street. Listed on the New York Stock Exchange under the ticker CRCL, the company raised $1.05 billion by placing 34 million shares at $31 each, for a valuation of $6.9 billion. The deal, orchestrated by J.P. Morgan, Citigroup and Goldman Sachs, caused an immediate stir, with the stock jumping 168% in its first trading session.

>> Circle and Coinbase: the secrets of a $172 million-a-year pact

Two months later, it was Bullish that caused a stir. Initially planned for 20 million shares, its offer was raised to 30 million, with a final price set at $37 per share. The result: $1.11 billion raised and a share price that opened at $90 on 13 August, before climbing to $118 in a highly volatile session.

At the same time, the market saw several other major deals emerge. ProCap Acquisition Corp, a SPAC launched by Anthony Pompliano, raised $250m when it floated on the Nasdaq in May. A few weeks later, Amber International, a subsidiary of Asia's Amber Group, floated on Nasdaq via a merger with iClick Interactive Asia Group. Renamed AMBR, the share jumped 19% on its first trading day.

September saw two closely watched IPOs. First was Gemini, which raised its price range before placing 16.6 million shares at $28. GEMI shares opened at $37 and closed at $32, reflecting strong demand despite high volatility. Then there was Figure Technology Solutions, which raised $787.5 million at an initial valuation of $5.3 billion. Its FIGR shares quickly gained 24% in the first session, pushing its valuation to around 6.6 billion.

>> Gillian Lynch (Gemini): "We're coming to France at the best possible time"

Galaxy Digital confirmed its place as institutional leader by announcing in May a subscribed offer of 29 million class A shares, including nearly 5 million from existing shareholders. Listed on the Nasdaq since 16 May under the ticker GLXY, the company is thus reinforcing its strategy of forging closer ties with the public markets.

Next candidates: BitGo, Grayscale, Kraken

On 21 July 2025, BitGo announced that it had confidentially filed a draft prospectus with the SEC. The number of shares and the price range have not yet been set, but the company, which claims more than $100 billion in assets under custody, intends to consolidate its role as a leader in institutional custody as the US regulatory framework becomes clearer.

A few days earlier, on 14 July 2025, Grayscale did the same. Founded in 2013, the platform has established itself as the world's largest digital asset manager, with a range of products from the Grayscale Bitcoin Trust (the first US-listed Bitcoin fund) to a series of cryptocurrency-indexed ETFs.

At the same time, exchange Kraken is positioning itself as one of the most eagerly awaited candidates. The company is aiming for an IPO as early as the first quarter of 2026, with a target of $500 million raised for an estimated valuation of $15 billion. This prospect was strengthened after the SEC dropped an action brought against it in March 2025, paving the way for a public listing.

In Europe, CoinShares is preparing for an arrival on the US Nasdaq via a merger with a special purpose acquisition company (SPAC). The deal, with Vine Hill Capital Investment Corp, would value the asset manager at around $1.2bn. The company, which is already listed in Stockholm, is thus looking to broaden its investor base and accelerate its international growth.

In the US, ConsenSys, the company behind MetaMask and Linea, is regularly cited as "IPO-ready". According to PitchBook, its IPO probability is estimated to be very high, although no official move has yet been confirmed.

>> Sharplink, the arm of Consensys and Linea

Ripple Labs is also among the names that come up often. However, chief executive Brad Garlinghouse has ruled out a listing in 2025, stressing that the company prefers to consolidate its operations and settle its legal disputes first. But a listing remains a possibility once the regulatory hurdles have been cleared.

Other companies are harder to pin down but come up regularly in conversation. Bitpanda in Europe, Ledger in France, Uniswap Labs, Anchorage Digital and Fireblocks in the US are among the most closely watched companies.

Crypto IPOs, a barometer of the market

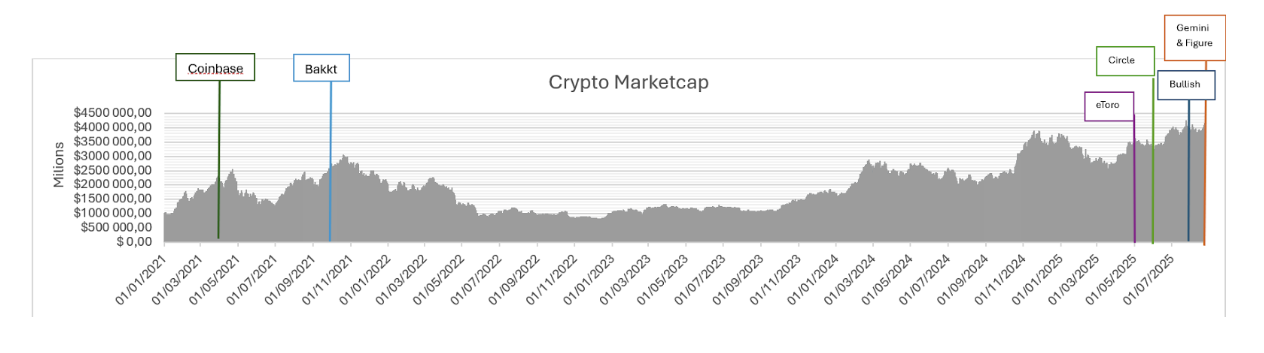

The timing of crypto-related IPOs says a lot about the cycles of the sector. The example of Coinbase, whose listing on the Nasdaq in April 2021 coincided with Bitcoin at its all-time highs, remains telling: that moment of high euphoria also saw Bakkt list on the NYSE and HIVE Blockchain join the Nasdaq.

Four years later, in 2025, a new wave of IPOs took shape. Circle, eToro, Bullish, Gemini and Figure Technologies took advantage of favourable market conditions to take the plunge. These deals are often concentrated in optimistic phases, when liquidity is abundant and investors are looking for increased exposure to digital assets.

In fact, IPOs function as a leading indicator of market sentiment. Companies choose to go public when they know they can maximise their valuation and attract capital. The trend is consistent with academic work on "IPO waves", which shows that they generally appear after strong stock market performances and in contexts of high confidence.

Valuation premiums that their traditional counterparts have never experienced

Crypto IPOs offer a contrast to those of traditional finance. Where Wall Street has long valued established models conservatively, companies linked to digital assets have often been floated with multiples that reflect growth potential (and speculation) more than fundamentals.

The case of Coinbase is emblematic. On 14 April 2021, its reference price had been set at $250 per share, giving a diluted valuation of $65 billion. But on opening day, the stock climbed to $381 and closed at $328, even peaking at $429, taking its capitalisation to nearly $86 billion. That's more than ten times its last private valuation of 8 billion, a symbol of the euphoria that reigned at the peak of the crypto bull cycle.

By way of comparison, Nasdaq Inc. at the time of its IPO in 2002 was valued at 1.18 billion dollars with a share introduced at 5 dollars.

PayPal also illustrates this more measured logic. In February 2002, its IPO raised $70 million for a valuation of $777 million. A few months later, eBay bought the company for 1.5 billion. When PayPal returned to the stock market in 2015 following its separation from eBay, its valuation had reached 47 billion dollars, surpassing that of its former parent company. At the time, the company processed $235 billion in annual payments and had 169 million users.

Two decades later, Circle has demonstrated an entirely different dynamic. Its IPO on 5 June 2025 was set at $31 per share for a valuation of $6.9 billion. At the opening, the share price jumped to $69 and ended the day at over $83, bringing the market capitalisation close to $18 billion. This deal, the first by a stablecoin issuer, confirmed that the markets are giving digital finance pioneers valuation premiums that their traditional counterparts have never experienced.

While players such as Nasdaq or PayPal have long been valued with restraint, reflecting the solidity but also the predictability of their models, Coinbase and Circle embody the opposite logic. The market has pushed their valuations to new heights by betting on their disruptive potential, even if this means putting their fundamentals on the back burner. A difference that underlines the extent to which speculative optimism still shapes the perception of crypto companies.

After the euphoria, the challenges of the market

The IPO is just the first step. Coinbase's experience bears witness to this: after a sensational IPO in 2021, its shares went through a long desert, rapidly falling back below their initial levels. It wasn't until July 2025 that the stock hit a new all-time high of $419.78.

In the meantime, the company has had to contend with volatile Bitcoin cycles, regulatory uncertainties and growing competition from both traditional finance and DeFi protocols.

This trajectory is not isolated. As Lex Sokolin, managing partner at Generative Ventures, points out, "the main lesson from Coinbase and Bakkt is the need to build solid fundamentals and diversify revenue streams". Too dependent on trading volumes or a single product, these players found themselves exposed to constant pressure on their valuations during bear market phases.

Crypto IPOs often reflect short-term enthusiasm, but their post-listing performance reveals a more complex reality. To hope to reassure investors over the long term, companies will need to demonstrate that they can withstand cycles and develop more resilient business models.

The example of Bakkt in turn illustrates the difficulties crypto companies have in maintaining investor confidence once listed. The company had chosen in 2021 the route of a merger with an SPAC, VPC Impact Acquisition Holdings, finalised on 15 October. Listed on the NYSE three days later under the ticker BKKT, it got off to a flying start: its shares briefly topped $42 after the announcement of partnerships with Mastercard and Fiserv.

But this euphoria was short-lived. The stock is now trading at around $9.50, a level that reflects the market's loss of confidence and limited returns for early shareholders.

Like Coinbase, Bakkt has suffered from an over-reliance on its crypto-asset business, which is particularly sensitive to price cycles. The decline in digital markets, coupled with lower-than-expected institutional adoption, has squeezed its revenues. Regulatory uncertainty in the US has added to this pressure.

Initial enthusiasm, fuelled by promises of rapid growth, quickly collided with operational reality.

EToro's track record also illustrates the limits of the crypto IPO craze. Introduced at $64.15, the stock is now trading at around $45, reflecting modest performance for investors.

Here again, dependence on trading volumes, exposure to particularly volatile markets and regulatory uncertainties have hampered growth. As with Coinbase or Bakkt, the gap between initial enthusiasm and operational reality quickly widened.

Formerly HIVE Blockchain Technologies, HIVE Digital Technologies won over the market when it was floated at around $13 per share. Four years later, the stock is trading at close to 4 dollars, a sharp decline that illustrates the difficulties encountered by this pioneer in "green" mining.

The company operates data centres powered by renewable energy, installed in particular in Bermuda, to mine cryptocurrencies and offer blockchain infrastructure solutions. But this strategy remains highly dependent on market cycles: the volatility of digital asset prices, combined with the high cost of such energy-intensive operations, weighs heavily on profitability. Added to this are regulatory uncertainties that make the company's trajectory more fragile.

The post-IPO performance of crypto companies is a reminder of the volatility and structural risks of the sector. Too often dependent on trading volumes, market cycles, high operational costs or a shifting regulatory framework, they struggle to deliver sustainable value to investors. The initial enthusiasm, which inflates valuations at the time of listing, quickly fades when the fundamentals do not follow.

For Aram Mughalyan, the trajectory of Coinbase and Bakkt speaks volumes. "Both entered in 2021, at the top of the cycle, buoyed by the hype. When the 2022 bear market came, they collapsed."

But what followed was different: Coinbase was able to reinvent itself, diversifying its revenues around subscriptions, asset custody, stablecoins via the USDC, or with the launch of its Base blockchain and associated app. As a result, the share price returned to all-time highs in 2025. Bakkt, on the other hand, has never really bounced back and continues to slide.

The moral, according to Aram Mughalyan, is clear: "The time for hype is over. You should go public when you have sustainable, profitable cash flow, not just because the market is buoyant."

IPOs, gateways to traditional finance

For crypto companies, going public represents much more than a simple change in status. It is a strategic lever that opens up access to substantial capital, which is essential for financing R&D, developing new infrastructure or accelerating expansion. Listing also gives the company greater visibility with investors, customers and partners, while providing an exit route for founders and early investors. Finally, it confers additional credibility, signalling to the market regulatory compliance, governance standards and transparency likely to appeal to institutional investors.

But this openness comes at a price. Independence is reduced, with managers having to report to their shareholders and to a board of directors. The transparency imposed by the market can expose operational weaknesses and force companies to focus on the short term to the detriment of long-term innovation. Added to this are high compliance costs and a dilution of control for founders.

For Lex Sokolin, however, the benefits of the liquidity of a listed market should not be overlooked: "The more liquidity, the better," he sums up, pointing out that the transparency and governance imposed by the market offer flexibility and choice to investors.

Aram Mughalyan agrees, believing that for centralised players, the constraints of the stock market are more than worth the benefits. "Reporting and audits buy the trust of counterparties, banks, asset managers and major fintechs", he notes, adding that a listed company also has an acquisition currency and easier access to capital.

This logic distinguishes centralised companies from decentralised protocols. The latter, via their tokens, are already "public" by nature, their code being open source and their metrics accessible on-chain. Conversely, centralised companies operate in an opaque fashion: the IPO then becomes a means of making up for this lack of transparency and bringing themselves up to the standards demanded by the financial markets.

The IPO acts both as a tool for integration and as a facade of respectability. It opens doors to traditional finance and gives crypto players credibility with institutional investors, but it does not in itself guarantee sustainability. This depends above all on sustainable business models, diversified revenues and the ability to balance investor expectations and strategic autonomy.

IPO or alternatives: the dilemma for crypto players

The traditional IPO is not the only route to the public markets. In 2021, SPACs (Special Purpose Acquisition Companies) became very popular, particularly with the example of Bakkt, which was floated via this mechanism. This process allows a private company to merge with a shell company that is already listed, thereby gaining faster and often cheaper access to the financial markets.

Several players, such as Circle and eToro, considered this option before giving up. But market volatility and tighter regulation quickly dampened the hype from 2022, leaving behind a tool with real opportunities, but surrounded by risks. For Lex Sokolin, SPACs remain valid: "They can work with any asset, crypto, fintech or otherwise."

Another avenue is emerging: the tokenisation of shares. This involves creating digital tokens representing traditional financial securities (shares, ETFs), backed 1:1 by real securities held by regulated custodians. These tokenised shares offer significant advantages: fractionalization, global accessibility, near-instantaneous settlements and continuous trading. Thanks to smart contracts, they add transparency, automation and cost reduction.

For Aram Mughalyan, the distinction is clear: SPACs are just a diversion to IPOs, with no real improvement in price discovery. Tokenisation, on the other hand, opens up a whole new field.

Tokenisation currently exists in two forms: 'native' tokenisation, which directly places on-chain shares in compliance with market rules (a model championed by Nasdaq, but still subject to KYC and strict permissions), and 'wrapper' tokenisation, where an on-chain token is backed by shares held off-chain by a custodian. The latter option, often without KYC, offers economic exposure but not always voting or direct shareholder rights. In the case of private shares, most tokens actually represent rights in an intermediary structure (SPV), with the issuer still able to block transfers on the cap table.

>> Tokenised shares: what's really behind this new trend