TBW - IPO: Can Ledger build on BitGo's success?

The success of BitGo's IPO this week on the New York Stock Exchange is recognition of the regulated custody model for digital assets. And behind this operation is already taking shape one of the major events of 2026: Ledger's IPO.

Positioned in the same segment, but with very different models and trajectories, the two players offer an illuminating field for comparison. This analysis looks back at what BitGo's IPO reveals and the lessons Ledger could learn from it as the markets approach.

BitGo: the premium for regulated infrastructure

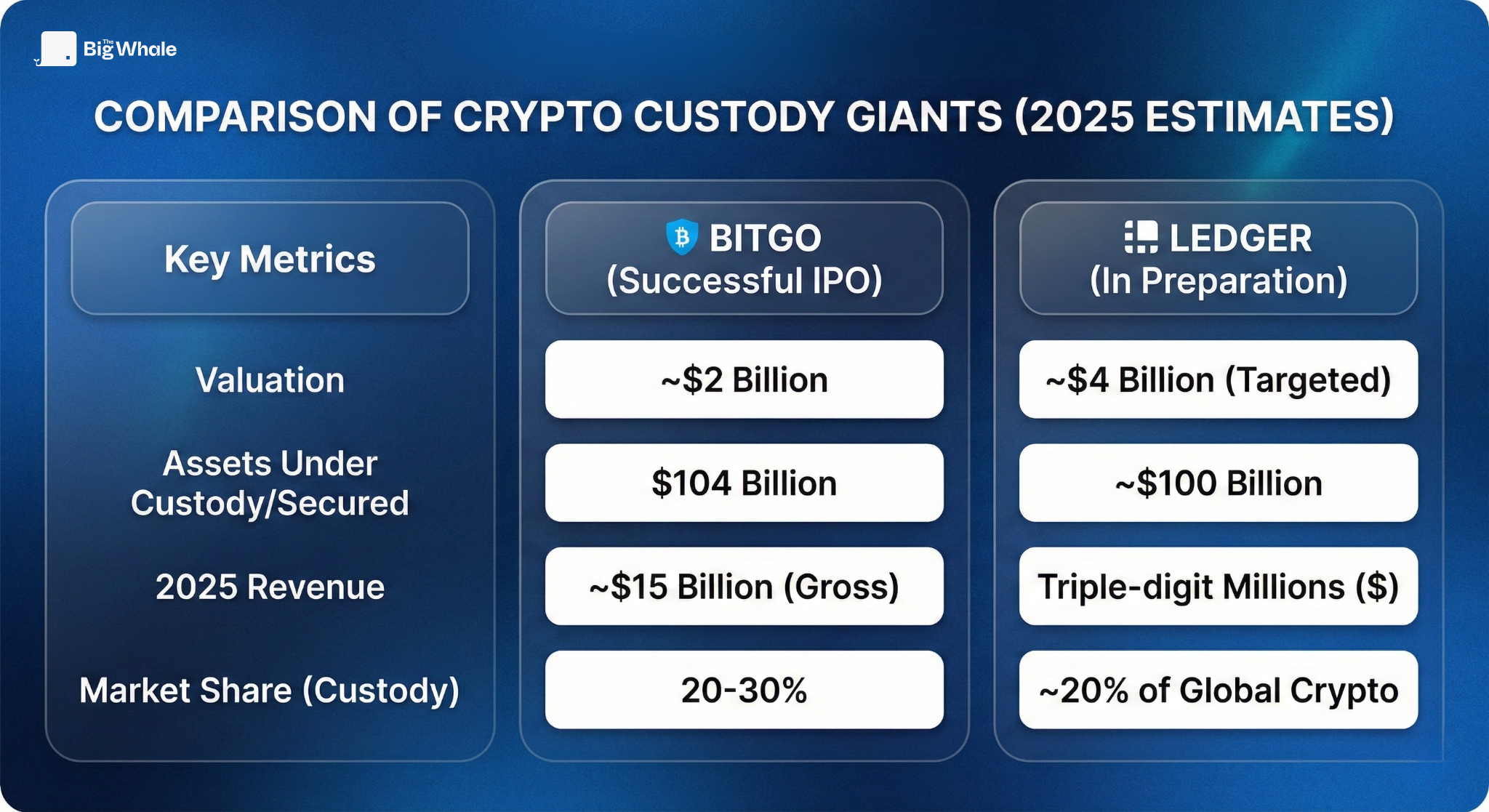

BitGo struck hard by setting its IPO price at $18 per share, above its initial range ($15-17), for a valuation in excess of $2 billion.

The figures reported by BitGo to the SEC prior to its IPO are rich in insight:

Explosion in revenue: in 2025, BitGo generated nearly $15 billion in revenue, compared with $1.9 billion over the same period in 2024.

The $15 billion revenue figure is not operational, but accounting-based. By expanding massively into Prime Brokerage and third-party trading, BitGo has changed the way the company accounts for its revenue. Unlike a traditional bank that only records its commissions, a platform acting as "principal" in a transaction can record the total value of the asset sold as revenue.

If expenses are removed, the "real" revenue would be much more modest (a few million).

Growth in assets under custody: its assets under management rose from $30.8 billion in 2024 to more than $104 billion in September 2025.

Profitability under control: despite massive investments in compliance and staff, BitGo posted a net profit of $35.3 million in the first three quarters of 2025.

The market has acclaimed BitGo because the company does not depend solely on trading volatility (like Coinbase), but on the recurrence of custody fees and infrastructure services (staking, settlement, etc.). It is precisely this base that Ledger is trying to consolidate.

BitGo relies on several technology partners to ensure the custody of its clients' assets, notably Thales. The American company does not develop its infrastructure end-to-end.

Ledger: from B2C to conquering Wall Street

If BitGo was born in the institutional cloud, Ledger comes from consumer hardware. But to aim for a valuation of $4 billion (the figure currently circulating for its IPO) the French unicorn has had to beef up its B2B offering (Ledger Enterprise) and above all its services (Ledger Wallet, formerly Ledger Live), which has led to a significant diversification of revenues in recent months.

Why Ledger's valuation could be higher than BitGo's

At first glance, BitGo appears to have a broader financial foundation, but Ledger has a unique advantage: technological sovereignty.

The ecosystem advantage: unlike a pure custodian like BitGo, Ledger controls both the hardware and software layers (Ledger Wallet/Enterprise). This vertical integration allows it to capture value at every stage of a digital asset's lifecycle.

The success of Ledger Wallet: the company offers a secure interface on which its clients can buy, sell, and generate yield (through partners like Kiln, Lombard, or Figment) from their digital assets. Each time, Ledger collects fees, enabling it to generate recurring revenue. According to our information, Ledger Wallet represents 50 % of the company's business.

The rise of Ledger Enterprise: while we don't know precisely what share of revenue Ledger Enterprise generates, several studies on hardware wallet manufacturers (Mordor Intelligence and SkyQuest) indicate that the institutional segment accounts for up to 30% of their activity (not confirmed).

In several recent appearances (notably in November 2025 and at Ledger Op3n), CEO Pascal Gauthier emphasized that the growth of the Enterprise division and recurring services (SaaS) is significantly higher than that of pure hardware. The management's stated goal is to transform Ledger into a "platform" whose revenues no longer depend solely on hardware sales cycles.

A unique technological choice: unlike Fireblocks, Taurus or DFNS (its competitors in the custody infrastructure segment), Ledger offers an HSM infrastructure that meets traditional cybersecurity standards.

The Big Whale's analysis

Ledger's IPO raises a risk management question: would you rather entrust your keys to a regulated third party (BitGo model) or own your own secure infrastructure (Ledger model)?

BitGo's success shows that public investors are hungry for "SaaS-like" dossiers in crypto, with predictable revenues and impeccable compliance. For Ledger, the challenge will be to prove that its hybrid model (hardware sales and recurring services via Ledger Enterprise) can maintain high margins.

>> Charles Guillemet (Ledger): "Wallets will replace passwords"