TBW - MARA: analysis of a high-voltage strategy

The essentials

- A structural pivot: MARA is emerging from all-mining to become a hybrid conglomerate (AI, energy infrastructure) and a "Bitcoin treasury company" (53,000 BTC).

- Financial fragility: Behind book profits driven by asset valuations, the group is burning through operating cash and financing its growth through dilution.

- European offensive: The acquisition of Exaion (EDF) would mark a strategic shift towards high-performance computing (HPC) powered by French nuclear energy.

Brief history of MARA

Today ranked among the world's largest listed bitcoin miners by market capitalisation, Marathon Digital Holdings, better known as MARA, has not always been a crypto company, however. Founded in 2010 under the name Marathon Patent Group, the company initially operated in an entirely different sector: the valuation of intellectual property patent portfolios. At the time, its model was based on the acquisition of patents relating to encryption technologies, exploited via its subsidiary Uniloc, mainly for litigation purposes targeting major technology groups.

The shift towards bitcoin began in 2017, but it was really from 2020 that the transformation became structural. That year, Marathon acquired its first S19 Pro mining machines from Chinese manufacturer Bitmain, financed out of its own funds. The company then signed a major contract with Bitmain to gradually increase its fleet to more than 103,000 S19 and S19 Pro machines, representing a theoretical capacity of 10.36 EH/s by the end of 2021.

In April 2021, the arrival of Fred Thiel at the head of the group marked a new stage in this strategy, accompanied by the change of name to Marathon Digital Holdings and the adoption of the $MARA stock market ticker.

Between 2022 and 2023, the company accelerates its international industrial expansion, structuring a global network of data centres and emphasising the integration of alternative energy sources to reduce its carbon intensity.

In December 2023, Marathon crosses a new threshold by acquiring two mining production sites for almost $179 million. At the same time, the group is investing in the optimisation of its operational chain with the development of proprietary solutions, such as its 2PIC immersion cooling system, its MARAFW firmware, but also blockchain infrastructure bricks such as Anduro, a Bitcoin-backed sidechain, or Alys, compatible with the Ethereum ecosystem.

At the end of 2023, Marathon is also experimenting with new growth drivers by deploying its first ASIC equipment dedicated to the Kaspa network.

In the wake of the explosion in artificial intelligence and the global demand for computing power, MARA, like a large part of the mining sector, is taking a closer interest in the high-performance computing (HPC) segment. This diversification is being supported in particular by a $250 million convertible bond issue, designed both to boost its computing capacity and to continue accumulating bitcoin on its balance sheet.

In the first half of this year, a major strategic shift took place: Marathon explicitly began its transformation into a "Bitcoin treasury company". To finance this new direction, the group raised almost $950 million in new convertible bonds.

A development that now positions MARA not just as an industrial player in mining, but as a financial vehicle with direct and growing exposure.

>> Bitcoin Mining: A profitable but only-for-the-powerful industry

Future development plan

The history of MARA reveals a succession of rapid, sometimes opportunistic, strategic pivots that have profoundly transformed its business model. Today, the group operates simultaneously in three particularly capital-intensive businesses with volatile margin profiles: bitcoin mining, high-performance computing (HPC/IA) and the management of massive cash holdings in bitcoin. An atypical configuration, at the frontier between the energy industry, digital infrastructure and financial strategy.

The ambition now on display is clear: MARA wants to move beyond its status as a simple miner to become a vertically integrated player in computing infrastructure and digital assets. Mining has not been abandoned, but it is set to become part of a broader strategy combining energy production, computing power and the financial monetisation of the bitcoin balance sheet.

At the same time, management intends to actively develop return strategies on its BTC reserves, via "bitcoin yield" products integrated into its financial architecture.

Mining remains an industrial pillar

On the mining segment, MARA still has very significant growth ambitions. The group plans to increase its hash capacity from the current 60 EH/s to 75 EH/s by the end of the year.

A ramp-up that would require an estimated $150 million in additional investment. Despite the cyclical nature of the sector, the company is thus confirming that mining remains a strategic foundation, both as a source of direct bitcoin production and as a tool for enhancing the value of its energy infrastructures.

To improve the economic efficiency of its operations, MARA has also announced a structuring partnership with MPLX aimed at integrating power generation and data centres. The project starts with 400 MW of capacity backed by a gas pipeline infrastructure, with the potential to scale up to 1.5 GW. Located in West Texas, the complex is intended to enable the company to arbitrate dynamically between mining activities and high-performance computing uses, depending on market conditions, energy prices and demand for computing power.

AI and HPC move to the forefront

The forthcoming acquisition of Exaion (subject to the French government approving the purchase of the subsidiary of electricity giant EDF) marks a decisive step in MARA's strategy of diversifying into AI and HPC. The deal involves the takeover of up to 64% of the capital for around €168 million, together with an exclusivity clause prohibiting the former shareholder, EDF, from any future activity in advanced computing.

This transaction enables MARA to establish a direct foothold in Europe in a strategic high-growth segment, while securing immediately operational industrial capabilities.

>> Rachat d'Exaion par MARA : This clause that deprives EDF of computing for AI and Bitcoin

In the United States, the group is also planning to deploy ten AI inference racks at its Granbury, Texas site, using its proprietary 2PiC immersion cooling technology to optimise energy efficiency. Commissioning is expected in 2026.

After raising $950 million via convertible bonds in the summer of 2025, several analysts are now projecting sales close to $1.1 billion by 2028, with an average annual growth rate of around 12% and a return to positive free cash flow.

As a sign of the growing importance of this business, MARA has announced that the financial performance of the IA/HPC segment will henceforth be published separately from the fourth quarter of 2025. A decision that establishes this segment as a central axis of the Group's future business model.

A bitcoin treasury strategy now accepted

As of 17 November 2025, MARA held 53,250 bitcoins, making it the second largest listed bitcoin treasury company in the world.

A notable feature compared with its peers: the group claims an active strategy of putting its reserves to work, via loans granted to counterparties deemed to be very solid in terms of credit risk.

A more marginal proportion is also dedicated to trading operations. According to several sources, around 14% of reserves (i.e. almost 7,400 BTC) are currently committed to these return-generating strategies.

Although this is no longer the strategic priority, MARA will continue to mine bitcoin and gradually build up its stockpile over the course of 2026. The management of this cryptoasset balance sheet is thus becoming a genuine financial business in its own right, at the heart of the Group's stock market valuation.

When asked about the group's dominant focuses, Alexandre Schmidt, equity index manager at CoinShares, sums up the situation as follows: "MARA today combines energy production via the MPLX partnership, development of AI inference offerings with the integration of Exaion, maintenance of a fast-growing mining fleet, and management of a cash position in bitcoin that now represents almost $4.5 billion. A rare combination, blurring the traditional boundaries between industrial infrastructure, tech and market finance."

Financial health

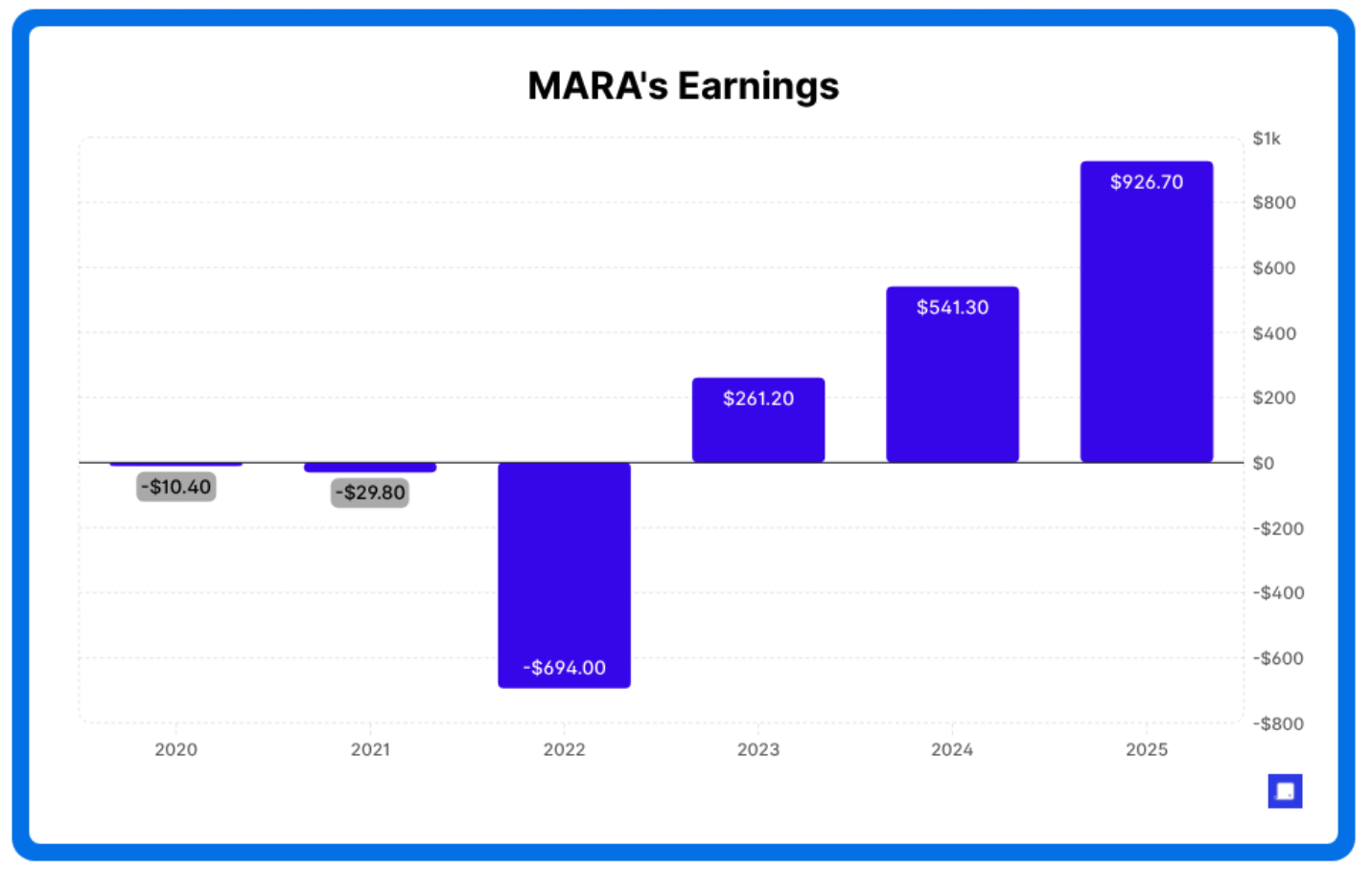

On paper, MARA has been posting profitable results for several financial years. But the recent stock market trend is a stark reminder that the market remains cautious about the group's financial solidity.

In the space of a month, the share price has lost almost 50%, a sign of marked investor mistrust. Over the last twelve rolling months, however, net profit came to $926 million, a clear improvement on the low point of the previous down cycle.

However, this growth needs to be put into perspective. In 2024, net income jumped by almost 73% compared with 2023, but most of this performance came from items classified as "other non-operating income".

These are mainly changes in the fair value of bitcoins held on the balance sheet, interest income related to lending activities, and items with no direct link to industrial mining or high-performance computing activities. Most of these gains have not been cashed in. They do not generate operating cash flow and mask a much tighter reality in terms of cash flow.

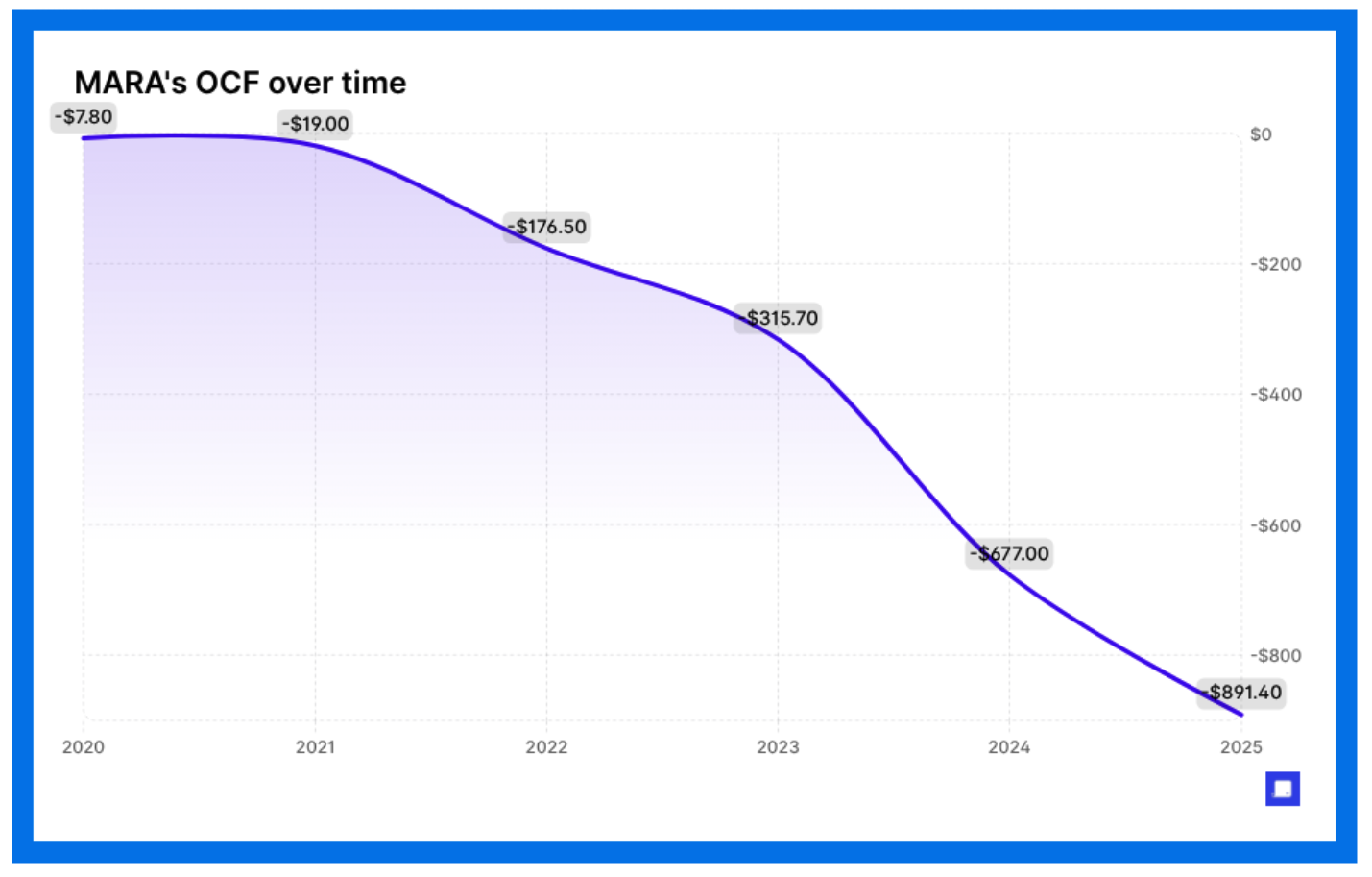

Operating cash flow remains deeply in the red, with a cumulative deficit of nearly $891 million. This is compounded by massive capital expenditure: nearly $877 million in capital expenditure over the recent period. All in all, MARA has a very high cash burn, characteristic of a model that is still in the construction phase and highly dependent on financing cycles.

This situation is directly reflected in the structure of the balance sheet. The debt-to-asset ratio is now around 40%, compared with significantly lower levels in recent years. Over the last twelve months, the Group's total debt has risen by more than a billion dollars to around 3.6 billion dollars. However, with negative operating cash flow, the company's intrinsic ability to service debt from its core activities remains limited, even if the average cost of debt remains relatively moderate at around 1.7%.

In this context, there is little room for manoeuvre. In the short and medium term, realistic options boil down to renewed recourse to debt to refinance existing maturities, or to new operations that dilute shareholders' equity. This cocktail is fuelling questions about the Group's strategic clarity, increasing the perception of risk and exerting lasting pressure on the share price.

A heavily discounted valuation that already incorporates a lot of risk

However, not everything is negative for shareholders over a multi-year horizon, provided that the pivot towards AI and high-performance computing materialises industrially and commercially. At this stage, the share is trading at historically low multiples. The price to sales ratio stands at 4.51, with a forward-looking multiple of close to 4.7, well below the five-year average of nearly 60. Put another way, the market is applying a discount of around 92% to the group's historical standards, which theoretically suggests very significant potential for revaluation if the new model is validated.

The price to earnings ratio illustrates the same asymmetry. The P/E on past earnings is around 5.6, while the projected P/E is 14.7. These levels reflect a high degree of caution on the part of investors, who remain more in a "growth option" mindset than in a traditional reading of established value.

The most optimistic projections are for sales from the HPC division to be close to $1.1 billion by 2028, based on an annual growth rate of around 12.5% over three years. Discounted to today, this trajectory represents nearly 770 million dollars, or almost double the Group's current revenues. But this assumption assumes smooth execution in an extremely competitive sector.

Debt: a risk that is still under control, provided that the strategy is clarified

When asked about the weight of debt in MARA's stock market momentum, Alexandre Schmidt (CoinShares) was relatively measured: in his view, "debt is not, at this stage, the main risk factor for the group". He even believes that MARA still has the capacity to take on more debt to accelerate its investments, if it so wishes. "But on one essential condition: to clarify its strategic priorities quickly."

"While the competition communicates massively about its data centre projects dedicated to AI, MARA remains more discreet about its concrete industrial ambitions in HPC. Yet it is precisely this type of announcement that has been the main driver of stock market rises for the major mining companies in recent months. As long as this visibility remains limited, the stock's trajectory should remain constrained, despite an apparent discount that has become significant."

Causes of the criticism

MARA is currently one of the bitcoin mining players most criticised by the markets. This is due to a combination of factors that have led to the group's business model and governance being repeatedly called into question. Structurally weak cash flows, massive shareholder dilution through successive share and convertible bond issues, sometimes questionable operational execution and, above all, a lack of strategic clarity.

All elements that explain why the stock remains under pressure despite the favourable momentum of the crypto sector over the long term.

Since its definitive shift towards Bitcoin and mining, MARA gives the impression of a group in perpetual reinvention, moving from one strategic narrative to another as market cycles dictate. Mining, bitcoin cash, and now artificial intelligence and high-performance computing: each phase corresponds to a new narrative, often in line with the 'narrative of the moment'. While this ability to adapt may be seen as an asset, it is above all interpreted by a large proportion of investors as a lack of structuring direction.

Or, the markets place a low value on strategic indecision, which is directly reflected in the group's stock market trajectory.

Technical controversies and a tarnished image in the Bitcoin ecosystem

In addition to financial issues, MARA has also attracted fierce criticism from within the Bitcoin ecosystem itself. In particular, the group has been criticised for inserting arbitrary data into the blocks it mined via its own pool, MARA Pool, in return for additional fees. Thanks to its so-called "slipstream" function, the company allows third parties to include this type of data for a cost of 10 sats per vByte, i.e. around five times the average peer-to-peer network rate.

Combined with the removal of the historical OP_RETURN limit, this practice led MARA to mine blocks containing non-essential data, described by some players as "polluting" the blockchain, turning the blocks into receptacles for content with no functional use for the network. Even if the operation is economically rational from a strictly financial point of view, it has permanently damaged the group's image in the eyes of part of the community and certain investors sensitive to the protocol's governance issues.

The Exaion affair and the question of competition

The takeover of Exaion in Europe has also given rise to strong tensions. The inclusion of a non-competition clause imposed on EDF as part of the deal was the subject of fierce criticism. Some saw it as an attempt to lock in French capabilities in Bitcoin mining and high-performance computing for the long term, while eliminating a potentially competing public player.

This "extra-financial" dimension has rekindled questions about MARA's long-term strategy and its methods of expansion outside the US.

Investors see communication as too conceptual

For Alexandre Schmidt, equity index manager at CoinShares, the heart of the problem remains above all the legibility of the industrial project. In his view, "the current lack of confidence is mainly due to the lack of clarity and tangible results from the various initiatives announced in recent years". MARA would give "the image of a company without any real short- and medium-term catalysts, despite the multiplication of partnerships".

"When the group communicates, for example, about contracts likely to generate a few million dollars in revenue, the first question investors ask is that of concrete execution: how will this activity actually materialise in the accounts?" The speeches made by management, and in particular by CEO Fred Thiel, are often perceived as highly visionary, highly conceptual, but insufficiently anchored in precise operational indicators.

Or, in a market environment that has become selective once again, investors are above all looking to understand what the teams "on the ground" are actually producing, rather than a theoretical twenty-year projection of how society or the uses of AI will evolve. "Companies built purely on a long-term story, with no rapid materialisation in figures, are now seeing their valuations heavily discounted. MARA is now fully experiencing this."

Why MARA is looking to Europe

MARA's interest in Europe is based above all on a very rational industrial and economic equation: an abundance of low-carbon energy at competitive cost, combined with the existence of high-level computing infrastructures, accessible at a valuation deemed attractive. The potential acquisition of Exaion for around €168 million, with options bringing the potential investment to almost a further €127 million, is precisely in line with this strategic arbitrage rationale.

By choosing Paris as its European bridgehead, MARA is anchoring itself at the heart of a country with both a massive nuclear fleet, an extremely robust electricity grid, and a political positioning favourable to the development of energy-intensive activities, such as inference computing for artificial intelligence.

The Exaion deal would also provide MARA with immediate access to very high-level data centres that comply with the European regulatory framework for data protection (RGPD) and are classified as Tier IV, with a theoretical availability rate of 99.995%. This level of reliability is a prerequisite for high value-added AI inference activities, which require ultra-resilient infrastructures. At the same time, the partnership with EDF will enable energy costs to be cut by around 20%, further strengthening the site's economic competitiveness in relation to international standards.

MARA's European strategy is more broadly in line with continental policies on decarbonisation and energy transition. The increase in public investment in low-carbon energy, networks and production capacity is creating a favourable environment for the establishment of new-generation computing centres. MARA intends to position itself on this wave by acquiring or directly operating these energy and digital infrastructures, in order to capture their value over the long term.

Facing a global race in high-performance computing now dominated by players such as IREN and Core Scientific, MARA's management is setting its sights very high in Europe. The group is talking about an investment programme of up to five billion dollars in France and continental Europe over the next five years. A trajectory that, if it materialises, would make Europe one of MARA's main strategic growth drivers outside the US.

The Big Whale's opinion

The bitcoin mining sector is undergoing a major transformation. Under pressure from competition, volatile energy prices and the rise of high-performance computing, miners now have no choice but to constantly optimise their infrastructures and margins. MARA is no exception to this dynamic and, in many respects, is behaving like its peers. But where this constant adaptation becomes problematic is when the market perceives excessive strategic dispersion.

By seeking to simultaneously occupy the position of industrial producer of bitcoins, operator of HPC infrastructures, AI player and "Bitcoin treasury company", MARA gives the impression of trying to sit on too many chairs at once, in an environment where each of these activities requires considerable amounts of capital. This fragmentation of the model, combined with persistent operating losses, means that the company is structurally dependent on external financing. The massive recourse to convertible bonds and shareholder dilution then becomes less a lever of opportunity than a tool for financial survival to support each new growth relay.

Like any listed company, MARA is guided by the pursuit of profit. But when this quest is accompanied by a logic where "the end justifies the means", the market's gaze becomes decidedly more critical. Accounting profitability, largely fuelled by balance sheet valuation effects, is no longer sufficient to compensate for the lack of recurring and predictable cash generation. In an environment where investors are now focusing on execution, financial discipline and visibility, MARA's trajectory is still perceived as fragile.

In other words, there is real potential, particularly in high-performance computing and the valuation of the balance sheet in bitcoin. But until the group demonstrates its ability to transform its ambitions into tangible and sustainable cash flows, the discount applied by the market will continue to reflect, above all, a lack of confidence.

* When contacted, Mara did not wish to answer our questions prior to the State's decision on the acquisition of Exaion.*

>> Check out our Bitcoin Dashboard

>> Briefing: the state of Bitcoin in Q3 2025