TBW - The crypto strategy of Stripe, the new giant in the sector

Since its first trials with bitcoin in 2014, Stripe has always kept a close eye on crypto-assets as payment methods. After dropping support for BTC in 2018, the US company has relaunched its strategy, this time betting on stablecoins. The acquisition of startup Bridge for $1.5 billion marked a turning point.

The objective? Integrate stablecoins into its core business to expand its user base, increase its market share, and offer a simple and reliable crypto payment solution.

>> Download The Stablecoin Briefing (Q2 2025)

Overview of Stripe

Stripe operates in an ultra-competitive market with revenues that could reach $150 billion by 2030. Launched as a simple payment infrastructure, the company now generates most of its revenue from the fees charged on each transaction. But its range of services has expanded over time: invoicing (Stripe Billing), business creation (Stripe Atlas), fraud prevention (Stripe Radar), and more recently corporate treasury with Stripe Treasury, now enhanced by Bridge services.

The company also offers a non-custodial solution via the integration of Privy (acquired in June), to enable businesses and users to store their funds, take out loans or manage their exposure to various digital assets. All these services are available directly from the Stripe app.

Stripe's core business remains payment processing, but new products such as "Stablecoin Bills" (introduced via Bridge) or stablecoin cash management tools are strengthening its offering. Stripe plays a key role in today's digital economy, making it easier for businesses to integrate payments thanks to its easy-to-use interface for developers. The company positions itself as an intermediary layer between merchants and traditional payment networks such as Visa or Mastercard.

The integration of stablecoins and non-custodial wallets now allows Stripe users to choose an alternative value transfer layer, relying on public blockchains to exchange digital dollars, hedge against currency fluctuations, or send payments internationally.

Stripe charges a commission of 2.9%, plus a flat fee of $0.30 per transaction.

Stripe's strategy in digital assets

Stripe isn't just accepting payments in stablecoins. The company is seeking to make them a pillar of its financial infrastructure. Using its international network and existing partnerships, the fintech aims to connect merchants in underserved areas with major economies via stablecoins.

With this in mind, Stripe has launched its "Stablecoin Financial Accounts" in 101 countries. This global rollout is backed by the $1.1 billion acquisition of Bridge, one of the biggest M&A deals in the crypto sector. At the same time, Stripe also acquired Privy, a company specialising in wallet infrastructure to offer non-custodial solutions to its users.

These strategic choices have accompanied a very good 2024 for Stripe, with total payment volume (TPV) of $1.4 trillion, up 38% year-on-year. The entry into the stablecoin market is part of a global adoption dynamic, in a context where payment volumes on these new rails exceeded $27,000 billion in 2024.

For John Egan, head of crypto at Stripe, the turning point came after the first experiments with bitcoin: "We quickly realised that the volatility of BTC was not suitable for payment. It was stablecoins that changed all that. They finally make it possible to combine speed, accessibility and stability, qualities perfectly aligned with Stripe's initial mission: to simplify an inefficient global financial system. "

Acquisition of Bridge

The acquisition of Bridge has enabled Stripe to launch several key initiatives:

- Deployment of Stablecoin Financial Accounts

- Extension of use cases around stablecoins

- Response to the rise of PayPal with the launch of PYUSD

Thanks to this integration, Stripe customers can now use USDC and USDB stablecoins (stablecoin issued by Bridge) for payments, transfers and cash management.

The benefits? Instant settlements, reduced costs and global coverage for e-tailers. USDC transactions are possible on several public blockchains, offering near-instant finality, while retaining the advantages of decentralisation.

Beyond the current functionalities, the integration of stablecoins opens up new perspectives. Stripe now offers acceptance of stablecoin payments at checkout, with automatic conversion into fiat currency.

In the long term, this could lay the foundations for a proprietary layer enabling these assets to circulate on a large scale, and explore new use cases in decentralised finance (DeFi), particularly via the mobilisation of dormant funds in users' treasuries.

Acquisition of Privy

Alongside Bridge, Stripe has acquired Privy, a start-up specialising in crypto wallet access tools. This acquisition completes the user-side set-up:

- Product integration: Privy works as an independent product but is interoperable with the Stripe ecosystem. It enables simplified wallet creation, with a fluid experience, even for the uninitiated. Onboarding can be done in one click, while retaining a self-custody model.

- New use cases: Privy accelerates the bridge between crypto and fiat, useful for commerce, international transfers and trading. Prior to its acquisition, the tool had already processed several billion dollars worth of transactions. Combined with Bridge, it forms a complete infrastructure for "programmable finance": automated payments via intelligent agents, integration of DeFi services, etc.

- Strategic positioning: With these two acquisitions, Stripe is building its own "crypto stack", combining stablecoin infrastructure and wallet management. This is an important step in making the use of crypto-assets more accessible to all its customers, without taking them out of the Stripe environment.

Stripe's strategic conviction

Stripe's strategic conviction in crypto is based on a simple observation: global payments remain complex, slow and expensive. By focusing on stablecoins, the fintech aims to familiarise users with a faster, interoperable and accessible payment infrastructure, while laying the foundations for wider adoption of on-chain applications as the model evolves.

Rather than developing its own infrastructure, Stripe favours partnerships and targeted acquisitions, along the lines of its takeovers of Bridge and Privy. This approach enables the rapid integration of technological building blocks tailored to user expectations.

Returning to crypto since 2023, Stripe is moving forward cautiously, favouring stable assets such as USDC over Ethereum and Solana, and surrounding itself with reputable players.

The strategy is based on three pillars: regulatory compliance, ease of use and robust tools for businesses. For Stripe, the value of crypto lies not in ideology, but in its ability to make payments and commerce more fluid, provided it is integrated cleanly, without disruption.

Risks, uncertainties and challenges

But this ambition comes with several challenges. There are four types of risk: legal, financial, competitive and technical.

On the regulatory front, Stripe remains attentive to developments in the United States (where the GENIUS Act has not yet been definitively adopted) and in Europe, where the MiCA regulation imposes new requirements for transparency, AML compliance and transaction monitoring. In emerging countries, exchange controls add a further layer of complexity. And the relative anonymity of stablecoins is raising concerns among regulators, who are turning to KYC tools such as those from Privy.

From a financial perspective, stablecoins are not without risk. The USDC temporarily lost its anchor in 2023 when Silicon Valley Bank collapsed, a reminder that the model remains vulnerable to liquidity crises. The risk of a bank run remains structural.

The technical integration of Bridge and Privy also introduces new points of failure: potential flaws in the smart contracts, errors in key management, or the complexity of the user experience. Added to this are issues of scaling up or temporary unavailability of blockchains, which can affect users unfamiliar with the sector.

Finally, competition is intensifying. PayPal has launched its own stablecoin, PYUSD, from which it earns revenue on reserves and issue or redemption transactions, with potential returns of 3% to 4%. Block, for its part, has built an ecosystem around Bitcoin: hardware wallets, mining chips, and direct conversion of merchant revenues via Square. In a context where the bitcoin cash strategy is progressing, some companies are also looking to gain exposure to BTC.

For all that, Stripe does not see stablecoins as a threat. "On the contrary, it's an opportunity," explains John Egan, Stripe's head of crypto. "Historically, Stripe started with payments, then added invoicing, fraud prevention (Radar), business creation (Atlas) and cash management. Thanks to stablecoins, we can offer this complete package from day one, including to customers who didn't have access to it before."

Instead of focusing on lowering unit commissions, Stripe is banking on overall efficiency gains. Stablecoins eliminate exchange fees, bank network costs and interbank fees - which also weigh on Stripe. "A merchant in Argentina or Nigeria can lose a lot just to convert their currency, receive dollars or transfer funds. With stablecoins, these fees disappear. This allows us to both lower our fees and preserve our margins."

John Egan also highlights an emerging phenomenon: "micropaymentisation". In a world where intelligent agents interact autonomously, billions of micro-transactions could emerge - of 0.01 or even 0.001 cents. "These flows only make sense if the costs themselves are compressible. But stablecoins work on a percentage basis, with no minimum fixed cost. This opens the way to an economy of granularity, where volume compensates for low unit margins. And Stripe is well placed to support this shift."

Competition: facing PayPal and Block, a differentiated approach

Stripe is not alone in the niche of digital payments incorporating crypto-assets. Two strong competitors stand out: PayPal and Block, Inc.

PayPal has been active in the sector since 2020, when the company began offering its users the ability to buy, sell and hold cryptocurrencies via a partnership with Paxos. This partnership led to the launch of PYUSD, PayPal's stablecoin, backed by dollar reserves and issued by Paxos. Users can hold, send and receive PYUSD directly via the PayPal app, which also acts as an integrated wallet.

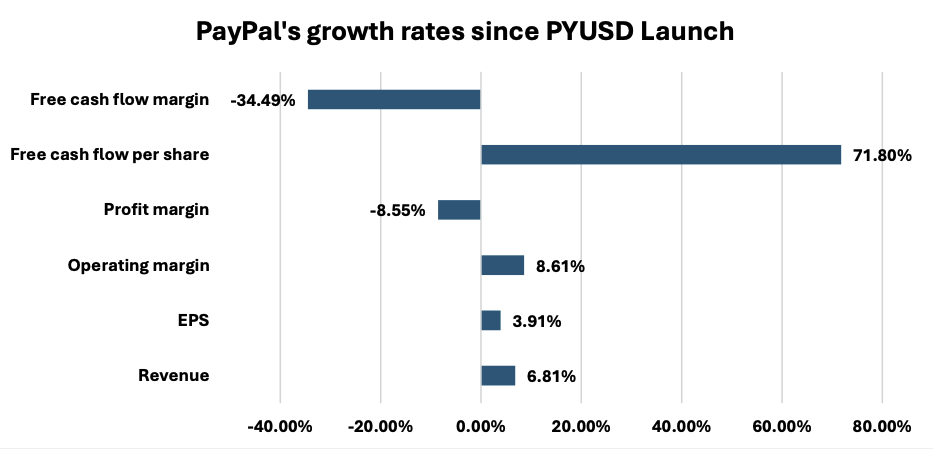

The introduction of PYUSD has enabled PayPal to monetise its reserves by cashing in on the interest generated, while benefiting from strong momentum on crypto adoption and growth in its key metrics: user acquisition, revenue, operating margins and cash flow per share.

Between 2020 and 2025, PayPal gained an additional 65 million users - up from the 185 million accounts it took the company 20 years to reach.

The adoption of stablecoin has benefited all indicators except net profit margins, affected in particular by slightly higher interest and tax expenses than in 2023.

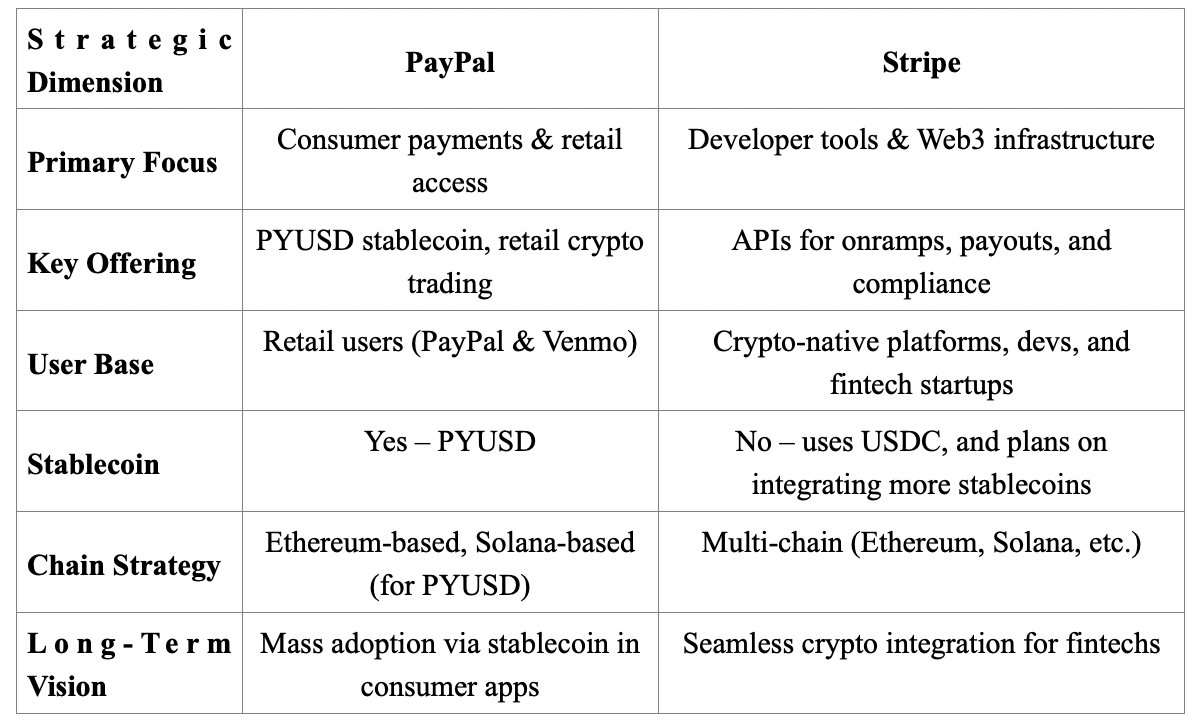

At heart, PayPal's strategy differs from Stripe's.

Where Stripe is aimed primarily at businesses, PayPal is targeting the general public. This focus allows PayPal to offer a return on the stablecoins held by its users.

By modulating the fees for issuing and redeeming PYUSD, the company can also make its solution more attractive against other stablecoins such as the USDC or USDT. This ability to adapt makes PayPal a potentially formidable player, both for individual users and for merchants interested in on-chain returns.

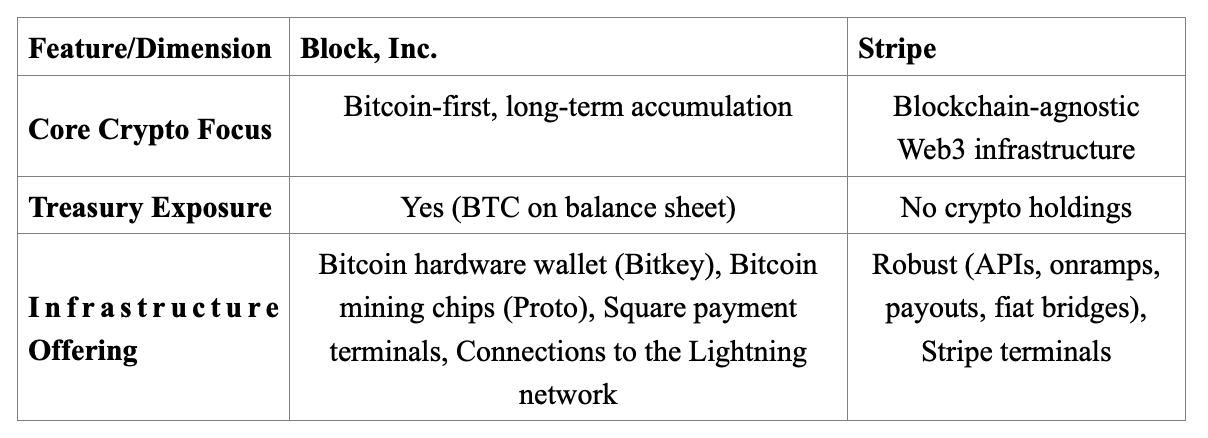

The second player to keep an eye on is Block (formerly Square), the company founded by Jack Dorsey. Unlike Stripe, Block is present both in the retail segment via Cash App and in the professional segment via Square, its payment terminal solution. The company is betting heavily on bitcoin, both in its cash strategy and in its service offering.

Block in particular allows merchants to convert part of their revenue into BTC, directly from their till. This option opens up access to bitcoin exposure for VSEs and SMEs, without going through traditional exchange platforms.

Block also continues to accumulate bitcoin as a reserve asset. The valuation of these reserves, combined with faster revenue growth than cost growth, has contributed to improved margins and earnings. Block is thus benefiting from the rise of Bitcoin as a cash asset, while offering direct integration of BTC into payment flows.

Against these two competitors, Stripe is defending a more cautious, B2B-oriented approach, based on stablecoin infrastructure and compliance. While PayPal is banking on the general public and the attractiveness of yield, and Block on exposure to bitcoin, Stripe is positioning itself as a provider of programmable payment solutions for businesses - with its sights set on the profound transformation of financial flows in the age of intelligent agents.

What's next? Stripe's next steps in crypto

Stripe has already laid the first bricks of a crypto strategy centred on stablecoins. But several avenues are reportedly being explored to go further: launching its own stablecoin, developing a dedicated blockchain infrastructure (such as a Layer 2-type layer), or even integrating on-chain yield products from DeFi.

Issuing an in-house stablecoin would allow Stripe to capture revenue from reserves, following the example of PayPal with PYUSD. The business model is particularly attractive, especially on the scale of a company that processes hundreds of billions of dollars a year.

Another avenue: creating an optimised Layer 2 Ethereum-type infrastructure layer, to reduce execution costs while retaining Ethereum's security and interoperability. Such a solution would allow Stripe to leverage the benefits of blockchain without relying on the high fees of the core network.

Finally, integrating yield products into the company's cash management could enhance the platform's attractiveness to customers. This could be done via the development of in-house tools or via partnerships with recognised DeFi protocols.

When asked about the possibility of working with players such as Morpho or Aave, Stripe's head of crypto, John Egan, does not close any doors: "As an international company with complex cash management needs, we have every interest in using protocols that provide real-time optimisation, dollar exposure and enhanced security. If the solutions are reliable, compliant and transparent, they should be integrated. But what interests us just as much is making them accessible to our customers. At Stripe, what we use internally often becomes a product in its own right. So it's very likely that we'll connect to protocols like Morpho, and offer these tools to our users, simply and securely."

>> Revolut chooses Morpho for its DeFi yield offer

The Big Whale's opinion

With a brand firmly established in the online payment sector and a presence in over 100 countries, Stripe has been able to forge partnerships with major players such as Visa and Shopify. Its payment volume now represents around 1.4% of global GDP, giving it the resources to invest in innovation via targeted acquisitions rather than building everything in-house.

His focus on stablecoins is consistent with its business model, based on optimising payment flows. But it also has its limitations. Stripe does not yet offer a clear solution for leveraging dormant stablecoin balances, for example via yield-generating protocols. Furthermore, until it has its own stablecoin, the company remains exposed to competition from PayPal and Block, but also from public blockchains that offer faster and cheaper alternatives.

Another possible barrier to adoption: fees. In addition to the commissions levied by Stripe, users also have to pay the network fees associated with stablecoin transactions. This could act as a brake on mass usage in certain contexts.

Despite these limitations, Stripe has implemented a crypto strategy that is logically in line with its DNA. The acquisition of Bridge and Privy gives it the means to act across the entire value chain, integrating stablecoins into its payment products as well as its treasury solutions.

It remains to be seen whether the company will go so far as to issue its own digital currency or build its blockchain infrastructure - which could take its crypto strategy into a new dimension.

>> Discover our dashboard dedicated to stablecoins