TBW - US vs. Europe: regulatory showdown over stablecoins

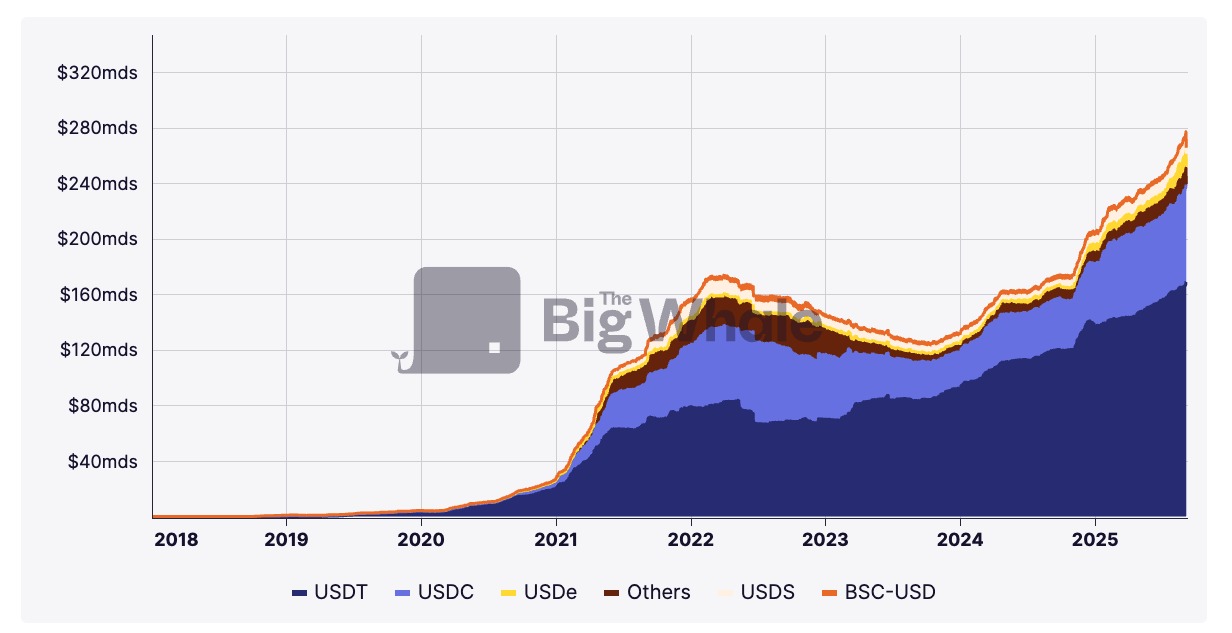

The stablecoin market continues to grow rapidly, driven by rising capitalisation and increasingly widespread adoption by major financial and technology players. Tether remains the undisputed leader, with a net profit of $4.9 billion recorded in the second quarter of 2025, proof of the intensity of demand.

On the fintech side, PayPal is leveraging its "Pay with Crypto" service to allow merchants to accept more than 100 cryptocurrencies, immediately converted into stablecoins such as PYUSD or fiat currency. Its in-house stablecoin, backed by the dollar at a fixed parity, acts as a bridge between cryptos and traditional payments, with reduced fees (up to 90% cheaper than bank cards) and near-instant liquidity for merchants.

Visa is following a similar trajectory. The payment giant is now integrating stablecoin payments into its network (USDC, EURC, USDG and PYUSD) and supporting more and more blockchains (Stellar and Avalanche, in addition to Solana and Ethereum). The aim is to strengthen interoperability and broaden usage within its ecosystem.

Specialised institutions are not to be outdone. Anchorage Digital has teamed up with Ethena Labs to launch USDtb, the first GENIUS Act-compliant stablecoin (read our analysis). Issued directly via the Anchorage platform, it targets US institutions, with the promise of a transparent and regulated framework.

This momentum is coupled with structuring initiatives. Circle marked the summer with its IPO and the launch of Arc, an EVM blockchain dedicated to stablecoin payments, foreign exchange settlements and capital markets. A special feature is that the USDC will serve as a native token for transaction fees, avoiding the need to create a separate token. The platform will also incorporate an FX engine for stablecoins and optional confidentiality functions. At the same time, Circle has become the first major global issuer to become fully MiCA compliant in the European Union, for both USDC and EURC.

"Circle's IPO and MiCA compliance marks a turning point for stablecoins and digital finance," summed up CEO Jeremy Allaire.

>> Explore our stablecoin dashboard

USA: a federal framework taking shape with the GENIUS Act and the Clarity Act

Washington stepped up a gear on the regulatory front this summer. Two major pieces of legislation have been passed: the GENIUS Act and the Clarity Act, which lay the groundwork for a unified federal framework for digital assets.

The GENIUS Act focuses on stablecoins. It limits their issuance to authorised entities (subsidiaries of insured banks or qualified non-banks) and requires 100% backing in high-quality liquid assets. The text also introduces transparency requirements for reserves, consumer protection measures and strict compliance with anti-money laundering rules. For the first time, clear standards will govern the granting of licences, the composition of reserves, redemption rights and the supervision of issuers. The aim is twofold: to reduce systemic risks while supporting innovation in digital finance.

The Clarity Act, meanwhile, answers another question that has been outstanding for years: which of the SEC or the CFTC should supervise the different types of crypto-assets? The text, supported by both parties, proposes a clear division of powers and aims to remove the uncertainty that has weighed on the sector since its inception.

At the same time, the SEC has launched the Project Crypto, a sign that the authority intends to maintain active oversight of the market and accompany its evolution.

The implications go beyond the regulatory framework alone. By requiring stablecoins to be backed by the dollar and governed by a federal scheme, the GENIUS Act also strengthens the place of the US currency in global finance. Stablecoins function as "digital exports" of dollars, increasing their use across borders.

The numbers bear this out: in 2025, Tether became the world's 18th largest holder of US Treasuries, with $127 billion in its portfolio. This growing exposure is helping to broaden the base of buyers of US debt and spread dollar liquidity internationally, while keeping control under US supervision.

The message is clear: in the US, the dollar intends to remain the default currency of the internet.

>> GENIUS Act and Clarity Act: The United States adopts 2 historic texts on cryptos

European Union : MiCA, a harmonised framework but still in its infancy

With the MiCA regulation, the European Union has created a single framework to regulate all crypto-assets, including stablecoins. The stated aim is to create a harmonised environment guaranteeing investor protection, market integrity and financial stability.

In contrast to a directive, MiCA is directly applicable in all Member States. However, its deployment is based on several levels: the competent national authorities, which issue authorisations and provide day-to-day supervision; ESMA, which is responsible for establishing technical standards and guidelines and coordinating the action of local authorities; and finally the European Commission, which steers delegated acts and overall policy.

For stablecoins, the text imposes strict conditions: full backing by liquid and very low-risk assets, mandatory authorisation of issuers, transparency and audit publication obligations, issue caps for certain electronic money tokens (EMTs).

These safeguards are intended to strengthen investor confidence and avoid any systemic risk, while allowing innovation.

The issue of regulatory overlap remains sensitive, however. On 10 June 2025, the European Banking Authority (EBA) published a "No Action Letter" clarifying the coexistence between MiCA and the Payment Services Directive (PSD2). It grants a transition period until 2 March 2026 to digital asset service providers (DASPs) that manage EMTs, temporarily exempting them from dual PSD2 authorisation, while maintaining certain key obligations (strong authentication, fraud reporting, capital requirements). The EBA ultimately recommends reform (via MiCA or a possible PSD3) to avoid duplication and ensure consistent supervision.

Several issuers have already obtained the MiCA sesame. These include Circle's EURC and USDC, Membrane Finance's eUSD and EUROe, Banking Circle's EURI, and Cryptocom's USD1 and SG-Forge's EURCV.

The list is expected to grow over the coming months as players become compliant.

Anatomy of stablecoin reserves: US vs Europe

The composition and management of reserves are at the heart of stablecoin profitability and strength. The American and European approaches, while converging on certain points, have notable differences that will have a direct impact on the way issuers structure their activities.

Who can issue?

In the United States, the GENIUS Act restricts issuance to "permitted stablecoin issuers", a category comprising three types of players: banks, non-banks approved by the Office of the Comptroller of the Currency (OCC), and state-authorised issuers, subject to managing less than $10 billion in outstandings.

In Europe, MiCA takes a broader approach. Article 2 covers any individual or company that issues crypto-assets, offers them to the public, admits them to trading or provides associated services. The text distinguishes two main categories of stablecoin:

- E-money tokens (EMT), backed by a single fiat currency (they are the most widespread, ed.).

- Asset-referenced tokens (ART), backed by a basket of assets (currencies, commodities, crypto).

The issue of reserves

The GENIUS Act imposes strict 100% coverage, with extremely liquid assets: dollars, insured deposits, Treasury bills with a maturity of less than 93 days, repos backed by these bills, or money market funds invested in sovereign assets. Any reuse of collateral (rehypothecation) is prohibited.

MiCA has a different framework.

- For ARTs (article 36), the EBA defines the liquidity rules: minimum percentage of bank deposits (30%), requirements by maturity, cash availability at 1 or 5 days, and a ban on reusing assets. Part of the reserves may be invested in liquid, low-risk instruments (government bonds, specialised UCITS funds). Gains or losses on these investments are the sole responsibility of the issuer, not the holders.

- For EMTs (article 54), at least 30% of the funds must be placed in segregated bank accounts, with the remainder in liquid and secure assets denominated in the same currency as the token.

Transparency and reporting

The GENIUS Act requires monthly publication of the composition of reserves and the number of stablecoins in circulation. Issuers exceeding $50 billion in assets must publish audited financial statements that are publicly available and provided to regulators.

Under MiCA, reporting is more frequent and more detailed for tokens exceeding certain thresholds. Article 22 provides for quarterly reporting for ARTs with outstandings in excess of €100 million, including the number of holders, size of reserves and transactional use. The authorities may also require such reporting below this threshold. Article 23 imposes issuance limits: if an ART exceeds 1 million daily transactions and a volume of 200 million euros in a currency zone, the issuer must suspend issuance and propose a corrective plan. These obligations also apply to EMTs denominated in non-European currencies.

Capital and risk management

The GENIUS Act requires issuers to hold sufficient liquidity at all times to meet redemption demands, and imposes reserve diversification.

MiCA sets more explicit capital requirements. Article 35 requires issuers of ARTs to maintain capital corresponding to the highest of three thresholds: €350,000, 2% of the average value of reserves over six months, or a quarter of the previous year's fixed costs. Significant EMTs are subject to the same rules.

Interest and yield

The GENIUS Act prohibits the payment of interest or yield to holders of stablecoins simply for holding them. However, it does not completely close the door to external schemes offered by third parties.

MiCA is stricter: sections 40 and 50 prohibit any form of remuneration, direct or indirect, linked to the holding of ARTs or EMTs. Even a rebate or commercial offer correlated to the holding period is treated as interest and therefore prohibited.

Supervision and audits

In the United States, supervision rests with the Treasury and the OCC, in coordination with state regulators.

In Europe, ESMA and EBA are the pivots of supervision, with a key role for national authorities. MiCA requires at least an annual independent audit of reserves for ARTs, and twice a year for significant issuers of EMTs.

Market size

In 2025, the global capitalisation of stablecoins amounts to $257.7 billion, or around 1.17% of the US M2 monetary aggregate. In Europe, the market remains modest: around €404 million in capitalisation for MiCA-compliant stablecoins.

GENIUS Act vs MiCA: two philosophies with an impact on profitability

The United States and the European Union now each have their own framework for regulating stablecoins. The GENIUS Act in the US and MiCA in Europe share the same objectives: financial stability, user protection, transparency and clear supervision. But their approaches diverge, and these differences have a direct impact on the profitability of issuers.

Two complementary but distinct visions

The GENIUS Act focuses exclusively on payment stablecoins, backed 1:1 against the dollar and issued by entities authorised in the United States. In this logic, stablecoins are treated as bank deposits, with reserves in cash or short-term Treasury bills.

In contrast, MiCA takes a broader approach, covering not only e-money tokens (backed by a single currency) but also asset-referenced tokens (backed by a basket of assets). The European regulation applies to all issuers and service providers operating in the EU, and also includes sections on market abuse and investor protection. Where the GENIUS Act prioritises the systemic security of the dollar, MiCA seeks to build a harmonised framework for the entire European crypto ecosystem.

The question of return

This is where the gap is widest.

- Under MiCA, Articles 40 and 50 formally prohibit any remuneration linked to the holding of stablecoins, including via affiliated third parties. The aim is clear: to maintain their function as a means of payment, without transforming them into investment products.

- The GENIUS Act also prohibits issuers from paying interest, but does not go so far as to regulate independent third parties. In practice, this leaves the door open to DeFi or fintech platforms that could offer a return on stablecoins, as long as the issuer remains outside the system.

Rentability: the transatlantic gap

This regulatory difference is reflected in the figures. As Chiara Munaretto (Stablecoin Insider) explains, "euro stablecoins must keep their reserves in low-yield bank deposits and liquid assets, spread across several institutions. This prudence limits room for manoeuvre and therefore profitability."

Sam Boboev (Fintech Wrap) agrees: "The US allows more flexibility in the allocation of reserves (cash equivalents, T-bills), while Europe favours security over income."

This rigour comes at a cost. For Lee A. Schneider (Ava Labs), "the stricter the rules, the lower the returns, and the more fragile the business model becomes". She also points out a paradox: by requiring European issuers to deposit a significant proportion of their reserves with banks, MiCA is de facto bringing stablecoins closer to a traditional banking model. In the event of a bank failure, it would be the State that would have to step in to guarantee repayment of the tokens - a logic reminiscent of bank deposits, despite the text's precautions.

How can euro stablecoins be made competitive?

This is the central question: how can euro-backed stablecoins compete with the USDC or USDT?

For Chiara Munaretto, "the EU should broaden the scope of assets eligible for reserves, while developing its capital markets to offer more liquidity and yield". Sam Boboev, for his part, insists "on the need to allow more investment flexibility and to clarify cross-border issuance mechanisms".

Today, the reality is contrasting:

- In the United States, the framework remains fragmented but pragmatic. Issuers can optimise their returns while relying on deep and liquid financial markets.

- In Europe, MiCA offers a comprehensive and harmonised framework, but its conservatism hampers profitability and could slow the adoption of euro stablecoins on a large scale.

Global competitiveness: the battle of regulatory frameworks

The regulation of stablecoins is no longer just being played out in Washington and Brussels. As the market matures, the world's major financial centres (from Singapore to Hong Kong) are imposing their own rules. These choices will have a direct impact on the competitiveness of currencies and the stablecoin ecosystems being built around them.

Growing fragmentation

The GENIUS Act in the US and MiCA in Europe have paved the way, but they are no longer alone.

- In Singapore, the Monetary Authority of Singapore (MAS) finalised in August 2023 a framework for stablecoins backed by a single currency (SCS), be it the Singapore dollar or a G10 currency. Issuers must guarantee full backing by liquid assets, maintain a minimum level of capital and ensure redemption at par within five business days.

- In Hong Kong, the Hong Kong Monetary Authority (HKMA) presented a comprehensive framework in July 2025: mandatory authorisation for issuers, dedicated supervision and specific anti-money laundering obligations. The system, which has been in force since 1 August 2025, is designed to provide a framework without curbing innovation.

These initiatives reflect a shared desire to make stablecoins usable as reliable means of payment while securing the ecosystem. But they also reinforce global regulatory fragmentation.

The cost of compliance

Compliance comes at a price, and it's not a trivial one. In Europe, nearly 45% of MiCA licence applications have already been rejected for non-compliance, and 42% of crypto start-ups anticipate a significant increase in their operational costs. Beyond licensing fees, compliance requires regular audits, constant reporting and enhanced operational monitoring.

This trend is not unique to the EU: everywhere, the rules involve heavy investment in legal and technical resources. For some players, the question is becoming strategic: stay within a strict jurisdiction to gain credibility, or migrate to a more flexible environment to preserve their margins and capacity for innovation.

A tension between innovation and supervision

The conclusion is clear: the global stablecoin landscape reflects a deep tension between stability and dynamism.

- The EU favours an exhaustive and protective framework, but at the cost of reduced profitability and a severe selection of candidates.

- The United States is moving forward with the GENIUS Act, which is more focused on the dollar and systemic risks, but leaves room for experimentation via the States.

- The United Kingdom is refining its system, with a stated desire to reconcile innovation and investor protection.

The result is a regulatory patchwork that increases complexity and costs for issuers. Without convergence, the risk is of a fragmented ecosystem emerging, with each currency developing in its own silo, to the detriment of global interoperability.

>> Explore our Stablecoin Briefing Q2